The biggest difference between Mutual Funds and NPS isn’t returns—it’s how and when you can use your money. Mutual funds offer flexibility for multiple financial goals, while NPS is designed specifically for retirement with strict withdrawal rules.

Imagine two friends who invest ₹10,000 every month for 25 years and earn similar returns. Everything goes according to plan until year 12, when one needs money to buy a house and the other faces a medical emergency.

The friend who invested in mutual funds can access the money within a few business days. The one who chose NPS discovers that most of the corpus remains locked until retirement.

That’s why comparing these two investments only on returns misses the bigger picture. Before looking at performance, you need to understand which one matches your financial goals, liquidity needs, and long-term plans.

Quick Summary: Mutual Fund vs NPS

If you’re short on time, here’s the biggest difference at a glance.

Evaluative Lens | National Pension System (NPS) | Mutual Funds |

Primary Purpose | Build a retirement corpus with long-term discipline | Build wealth for any financial goal |

Access to Your Money | Mostly locked until retirement, with limited withdrawal provisions | Money can usually be withdrawn within 1–3 business days (except ELSS) |

Investment Flexibility | Limited investment choices with regulated asset allocation | Wide variety of equity, debt, hybrid and index funds |

Equity Exposure | Active Choice allows equity exposure up to prescribed limits, reducing with age in Auto Choice | Can remain 100% invested in equity if you choose |

Additional tax deduction available under eligible provisions of the old tax regime | ELSS offers tax deduction, while other funds follow capital gains taxation | |

What Happens at Maturity? | Retirement withdrawal follows NPS exit rules, including annuity requirements where applicable | You decide when and how much to withdraw |

The right choice depends less on which investment earns more and more on what you expect your money to do for you.

What Is a Mutual Fund?

A mutual fund combines money from many investors and invests it in assets like stocks, bonds, or both. A professional fund manager handles the investments, so you don’t have to pick individual stocks yourself.

The biggest advantage of mutual funds is flexibility. You can invest for almost any goal, such as:

- Buying a home

- Your child’s education

- Building long-term wealth

- Early retirement

- Starting a business

- Creating an emergency fund

Unlike NPS, your money isn’t tied to retirement. You decide why you’re investing, how long you’ll stay invested, and when you want to withdraw your money.

That freedom is valuable, but it also requires discipline. Since your money is easy to access, you may feel tempted to withdraw it early instead of letting it grow over the long term.

What Is the National Pension System (NPS)?

The National Pension System (NPS) is a government-backed retirement scheme designed to help you build a retirement corpus. Unlike mutual funds, it’s meant only for retirement, so your money stays invested until you reach retirement age.

Your contributions are invested in a mix of equity, corporate bonds, and government securities to help your savings grow over time.

At retirement, you can’t always withdraw your entire corpus. If your corpus is up to ₹8 lakh, you can withdraw 100% tax-free. If it’s above ₹12 lakh (for eligible non-government subscribers), you can withdraw up to 80% tax-free, while the remaining 20% must be used to buy an annuity that pays you a monthly pension. This pension is generally taxable according to your income tax slab.

This is one of the most overlooked parts of NPS. Many people focus on the tax deduction when investing but don’t consider how they’ll receive their money after retirement.

The Control Conflict: Can You Access Your Money When You Need It?

This is one of the biggest differences between mutual funds and NPS.

With most mutual funds, you can withdraw your money whenever you need it, whether it’s for buying a home, paying for education, or handling an emergency. (The main exception is ELSS, which has a 3-year lock-in.)

NPS works differently. It locks your money until retirement to help you stay disciplined and avoid spending your retirement savings early.

In simple terms:

- Choose mutual funds if you want easy access to your money and are investing for goals before retirement.

- Choose NPS if your main goal is retirement and you prefer a system that keeps your savings locked away until then.

Neither is better than the other. The right choice depends on whether you value flexibility or long-term discipline more.

The Compounding Ceiling: Which Investment Gives Your Money More Room to Grow?

Both mutual funds and NPS are market-linked investments, but they invest in different ways.

With equity mutual funds, you can stay 100% invested in stocks for as long as you want, giving your money more room to grow over the long term. The trade-off is that you’ll also experience bigger ups and downs during market swings.

NPS follows a more balanced approach. Equity exposure is capped, and if you choose Auto Choice, it automatically reduces your stock allocation as you get older and moves more money into safer assets.

If you’re young and investing for decades, mutual funds may offer higher growth potential. If you’re close to retirement, NPS can help automatically reduce risk.

The key is to look beyond returns. Choose the investment strategy that matches your goals and risk tolerance.

The Tax Illusion: Saving Tax Today Doesn't Tell the Whole Story

Tax benefits are one of the biggest reasons people invest in NPS, but they depend on your tax regime.

If you’re under the New Tax Regime, you can’t claim the additional ₹50,000 deduction under Section 80CCD(1B). If you follow the Old Tax Regime, NPS can still help you save tax.

But don’t look only at the tax deduction. At retirement, a part of your NPS corpus may have to be used to buy an annuity, and the monthly pension you receive is generally taxable.

Mutual funds work differently. They usually don’t offer an upfront tax deduction (except ELSS), but they give you complete control over when and how you withdraw your money.

So, instead of asking, “Which investment saves more tax today?”, ask “Which one fits my financial goals better?”

Market Crash Stress Test: What Happens When Markets Fall?

Returns matter, but how your investment behaves during a market crash matters even more.

If you invest in an equity mutual fund, your portfolio can fall sharply when the stock market drops. Many investors panic and sell, turning temporary losses into permanent ones.

NPS works differently. If you choose Auto Choice, it gradually reduces your equity exposure as you get older and shifts more money into safer assets. This helps reduce risk as you move closer to retirement, although NPS can still lose value during market downturns.

Ask yourself one question: If your investment fell by 20% tomorrow, would you stay invested or sell? Your answer can help you choose the investment that’s right for you.

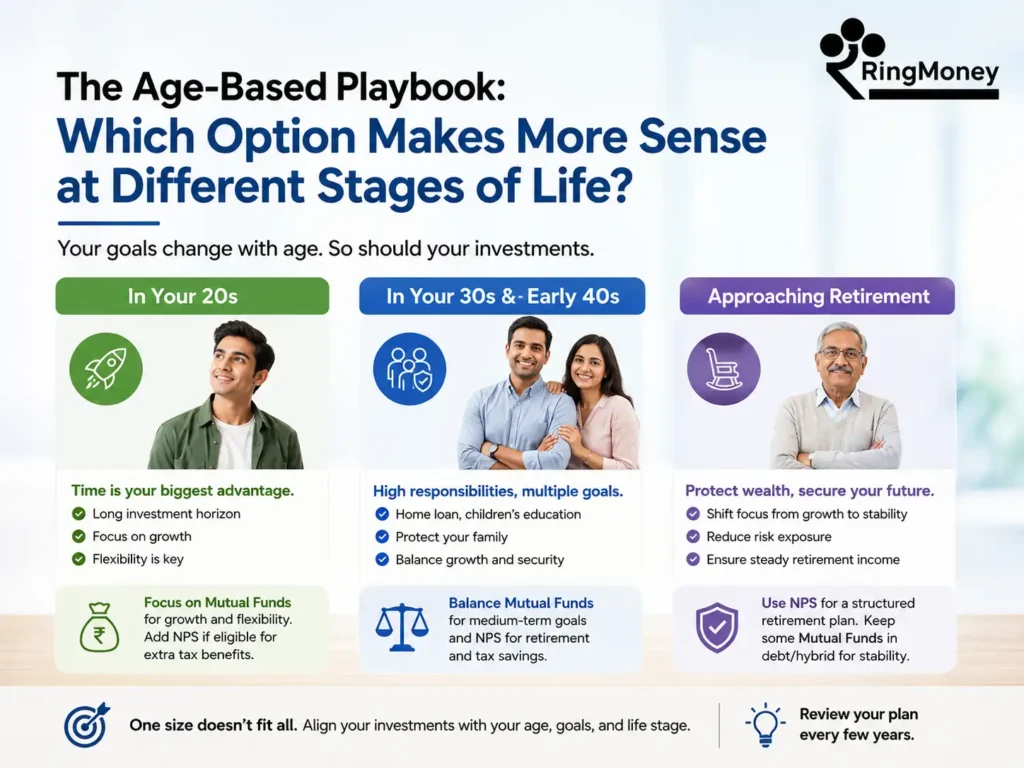

The Age-Based Playbook: Which Option Makes More Sense at Different Stages of Life?

There isn’t a single investment that works for everyone. Your priorities change as your career, income and responsibilities evolve.

If you're in your 20s

Your biggest advantage isn’t money—it’s time.

You have decades for your investments to recover from market downturns and benefit from long-term compounding. At this stage, flexibility is equally important because major life events are still ahead.

You may need money for:

- Higher education

- Marriage

- Buying your first home

- Starting a business

- Career changes

For many young investors, mutual funds become the primary wealth-building tool because they combine growth with liquidity. If you’re eligible for additional tax benefits, NPS can complement your portfolio rather than replace mutual funds.

If you're in your 30s and early 40s

This is often your highest spending phase.

Home loans, children’s education, insurance premiums and family responsibilities compete for your monthly income.

Instead of putting every rupee into a retirement account, many investors benefit from balancing both investments.

For example:

- Use mutual funds for medium-term financial goals.

- Use NPS specifically for retirement planning and eligible tax savings.

This separation helps you avoid dipping into retirement savings every time a major expense appears.

If you're approaching retirement

The focus gradually shifts from aggressive growth to protecting the wealth you’ve already built.

At this stage, NPS becomes more relevant because its structure naturally supports retirement planning. The gradual reduction in equity exposure also lowers the risk of a major market correction affecting your corpus just before retirement.

Mutual funds still have a place, especially debt and hybrid funds, but your overall asset allocation usually becomes more conservative.

Common Mistakes Investors Make

Most investment mistakes happen because people choose the right product for the wrong goal.

Investing in NPS only for tax savings

Many people invest in NPS just for the tax deduction without realising that their money stays locked until retirement. Make sure you’re comfortable with that before investing.

Using mutual funds without discipline

Mutual funds give you complete flexibility, but withdrawing money too often for lifestyle expenses can hurt your long-term wealth.

Looking only at past returns

Higher returns don’t always mean a better investment. Choose an option that matches your financial goals, not just its past performance.

Ignoring the exit rules

Many investors don’t check the withdrawal rules before investing. If you exit NPS before the age of 60, 80% of your corpus may have to be used to buy an annuity, leaving only 20% available as a lump sum. Understanding these rules can help you avoid surprises later.

Can You Invest in Both NPS and Mutual Funds?

Yes. In fact, for many people, combining both is a smarter strategy than choosing only one. Think of them as solving different financial problems.

Mutual funds help you build wealth for life’s milestones. NPS helps you create a retirement income that you are less likely to spend prematurely.

A balanced approach might look like this:

- Build an emergency fund separately.

- Invest through equity mutual funds for long-term wealth creation.

- Use NPS specifically for retirement planning and eligible tax benefits.

- Review your asset allocation every few years as your income and goals change.

Instead of forcing one investment to do everything, allow each one to perform the job it was designed for.

Which One Should You Choose?

The simplest answer isn’t “Mutual Funds are better” or “NPS is better.” The better investment is the one that matches your goal.

Use this checklist.

Choose Mutual Funds if you:

- Want flexibility to access your money.

- Are investing for goals before retirement.

- Want complete control over your portfolio.

- Can stay invested during market volatility without panicking.

- Prefer deciding when and how you withdraw your money.

Choose NPS if you:

- Want to build a dedicated retirement corpus.

- Struggle to stay disciplined with long-term investing.

- Qualify for additional tax benefits under the applicable tax regime.

- Prefer a structured investment that gradually reduces risk as retirement approaches.

- Want a retirement-focused investment separate from your other financial goals.

Consider both if you:

- Want long-term wealth creation and retirement security.

- Have enough monthly income to invest toward multiple goals.

- Don’t want retirement planning to interfere with other financial milestones.

For many investors, this balanced approach provides both flexibility and discipline without forcing an unnecessary compromise.

Frequently Asked Questions

Is NPS better than mutual funds?

Not necessarily. NPS is designed for retirement, while mutual funds can be used for almost any financial goal. The better choice depends on what you’re investing for.

Can you withdraw money from NPS anytime?

No. NPS has strict withdrawal rules, although partial withdrawals are permitted under specific conditions. Normal exit generally happens at retirement, subject to the prevailing regulations.

Which offers higher returns?

Neither product guarantees returns because both are market-linked. Equity mutual funds may have higher long-term growth potential due to greater equity exposure, while NPS follows a more balanced investment approach.

Is NPS safer than mutual funds?

NPS isn’t risk-free, but its regulated asset allocation and gradual reduction in equity exposure can make it less volatile as retirement approaches. Mutual fund risk depends entirely on the type of fund you choose.

Should you stop investing in mutual funds if you open an NPS account?

No. For many investors, both investments complement each other because they serve different financial objectives.

Final Thoughts

Before you decide, give yourself a quick score:

- Mostly retirement? → NPS is likely a better fit.

- Need money before retirement? → Mutual funds make more sense.

- Want both flexibility and retirement security? → Consider using both.

One final tip: don’t choose an investment just because it saves tax. Choose the one that matches when you’ll need the money. The best investment isn’t the one with the biggest tax break—it’s the one that helps you reach your financial goal.