Most people review their salary every year. Some even check their investments every week. But very few stop and ask themselves one important question: Am I still investing for the life I want today?

The simple answer is yes. If your goals have changed, your investments may need to change too. That’s because investments are only tools to help you reach a goal. Whether you’re saving to buy a house, retire comfortably, or pay for your child’s education, your investments should support that goal. If your goal changes, it’s worth checking whether your investment plan still fits.

Many investing mistakes don’t happen because someone chose the wrong mutual fund or invested at the wrong time. They happen because people continue following the same investment plan even after their life has changed. A portfolio that worked well a few years ago may not be the right fit for where you are today.

Your Investments Were Never the Goal. They Were Always the Vehicle.

It’s easy to become attached to your investments.

You might think, “I’ve been investing in this mutual fund for years,” or “This investment has given me good returns.” Over time, it’s natural to focus more on the investment itself than on the reason you started investing.

But your investments were never the goal.

They were meant to help you achieve important life goals, such as:

- Buying your first home

- Paying for your child’s education

- Building wealth for retirement

- Starting a business

- Becoming financially independent

- Leaving money for your family

Every investment should answer one simple question:

“What goal is this money helping me achieve?”

If you don’t know the answer, you may be investing out of habit instead of investing with a clear purpose.

Life doesn’t stay the same. Your priorities, responsibilities, income, and future plans can all change over time. A portfolio that suited you five or ten years ago may not be the right fit for your life today.

That’s why whenever your goals change, it’s a good idea to review whether your investments still support those goals.

What Happens When Life Quietly Rewrites Your Financial Priorities?

Most investment plans don’t become outdated because the market changes.

They become outdated because your life changes.

A promotion, marriage, having a child, buying a home, or caring for ageing parents can all change your financial priorities. These changes affect how much you can invest, how much risk you can take, and when you’ll need your money.

Here are some common life events that can change your investment plan:

Life Event | What Usually Changes |

Marriage | Shared finances, combined goals, different risk preferences |

Having children | Education planning, insurance needs, longer financial commitments |

Buying a home | Larger cash requirements and shorter timelines |

Career change or business | Income stability and emergency fund requirements |

Moving abroad | Currency exposure, taxation and future planning |

Early retirement | Investment horizon and withdrawal strategy |

Supporting ageing parents | Cash flow, liquidity needs and financial flexibility |

Notice that none of these is simply personal milestones.

Each one changes your timeline, your available cash flow, your financial obligations and your ability to take investment risk.

Your portfolio should reflect your current life—not your past life.

When your priorities evolve, your investments should have the opportunity to catch up.

Three Questions That Tell You Whether Your Investments Need an Update

You don’t need to review your investments every time the market moves.

Instead, ask yourself these three questions.

1. Has my deadline changed?

The timeline behind every financial goal matters.

Maybe you planned to buy a home in 10 years but now want to buy one in three. Or perhaps you’ve decided to retire later than planned.

Your time horizon has changed, and your investments should reflect that. An investment that’s suitable for a goal 20 years away may be too risky if you need the money in just two years. As your goal gets closer, protecting your money becomes more important than chasing higher returns.

2. Can I still afford the same level of risk?

Many people only think about risk tolerance—how comfortable they are with market ups and downs. But risk capacity is just as important. It refers to how much financial loss you can actually afford without affecting your goals or lifestyle.

Risk Tolerance | Risk Capacity |

How comfortable you are with market ups and downs | How much financial loss you can realistically afford |

Emotional | Financial and practical |

May stay the same | Often changes after major life events |

For example, you may still be comfortable taking investment risks after becoming a parent. But with more responsibilities and future expenses, your ability to recover from a big loss may be lower. That’s why you should consider both.

3. Do I still need the same return?

Higher returns aren’t always the right goal.

If your investment timeline becomes longer, you may not need to take as much risk because your money has more time to grow. If your goal is much closer, taking too much risk could put your savings at risk when you need them most.

Instead of chasing the highest returns, focus on the returns you actually need to achieve your goal. That’s why asset allocation is often more important than trying to pick the best-performing investment.

These Seven Moments Should Trigger an Investment Review—Not Market Crashes

Many investors review their portfolio only after markets fall sharply. In reality, markets don’t decide when your investments deserve attention.

Life does.

- Your annual financial review

Just as you schedule a health check-up, schedule a yearly investment review to ensure your portfolio still aligns with your current goals.

- A major life milestone

Marriage, a new child, purchasing a home, starting a business or planning retirement all deserve a fresh look at your investment strategy.

- A meaningful income change

Whether you’ve received a promotion, switched careers or experienced a temporary income reduction, your investment plan should reflect your new financial reality.

- Changes in debt

Taking on a mortgage, paying off education loans or reducing major liabilities changes both your monthly cash flow and your financial flexibility.

- Achieving one financial goal

Suppose you’ve successfully built your emergency fund.

Instead of continuing the same investment pattern automatically, ask yourself whether those monthly contributions could now be redirected towards retirement, education or wealth creation.

- Portfolio performance raises new questions

This isn’t about chasing returns. Instead, ask a better question:

Is this investment still helping me achieve the goal I originally bought it for?

A fund delivering excellent returns may still be the wrong fit if your timeline has changed dramatically.

- Your goal timeline changes

Perhaps retirement comes earlier than expected. Maybe buying a home gets postponed. Maybe higher education becomes a priority.

Whenever the finish line moves, your investment strategy deserves another review.

Changing Investments Doesn't Always Mean Starting From Scratch

One reason many people delay reviewing their portfolio is that they think they’ll have to sell everything and start over. In reality, that’s rarely necessary. Most portfolio updates involve small, thoughtful changes rather than a complete overhaul.

For example, you might:

- Gradually increase or reduce your equity allocation.

- Add more debt investments as a major goal gets closer.

- Increase your monthly SIP instead of changing your existing investments.

- Redirect future investments towards new financial goals.

- Rebalance your portfolio regularly to bring your asset allocation back in line with your goals.

The idea isn’t to rebuild your portfolio from scratch. It’s simply to make small adjustments so your investments continue supporting your current financial goals.

Signs You're Probably Investing on Autopilot

Sometimes, the biggest warning sign isn’t poor investment performance—it’s forgetting why you started investing in the first place.

See if any of these sound familiar:

- You’ve stuck with the same SIP: You haven’t reviewed whether it still matches your current goals.

- Your income has grown: But your investment amount hasn’t.

- Your family has grown: Yet you haven’t started investing for your child’s future.

- Your debt has changed: You paid off a major loan, but your investment strategy stayed the same.

- You’re investing out of habit: Some investments are still there simply because you’ve always had them.

- You’ve lost the purpose: You can’t clearly explain what each investment is meant to achieve.

If even one of these points applies to you, it’s a good time to review your portfolio.

Investing on autopilot may feel easy, but goal-based investing helps ensure your money continues to support the life you’re building.

The Biggest Investment Risk Isn't Market Volatility. It's Goal Misalignment.

Markets will always go up and down—that’s a normal part of investing.

A bigger risk is having a portfolio that no longer matches your financial goals. Even a well-performing investment may not be the right one if it no longer supports the purpose you originally invested for.

The goal isn’t to hold the same investments forever. It’s to make sure every investment continues helping you achieve the life you’re building.

Reviewing Your Investments Should Be Easy, Not Complicated

Knowing your investments need a review is one thing. Actually taking action is another.

Whether you need to increase your SIP, adjust your asset allocation, or start investing for a new goal, having the right platform can make the process much simpler. Instead of managing everything manually, choose a platform that lets you invest, track your progress, and update your strategy as your goals evolve.

With RingMoney, you can explore mutual funds, start or modify SIPs, and build an investment plan that grows with your changing financial goals. As your priorities change over time, reviewing and updating your investments becomes much easier, helping you stay focused on what you’re investing for—not just what you’re investing in.

Your Life Evolves. Your Portfolio Should Too.

Your financial goals won’t stay the same forever, and neither should your investment strategy. Changes in your career, income, family, or plans can all affect how you should invest.

Instead of reviewing your portfolio only when markets move, review it whenever your life changes. A simple check can help ensure your investments still support the goals that matter most to you.

Frequently Asked Questions

Should I change all my investments if my goals change?

Not necessarily. In many cases, small changes like adjusting future SIPs, rebalancing your portfolio, or changing your asset allocation are enough instead of replacing every investment.

How often should I review my financial goals?

A yearly review is a good habit, but you should also review your goals after major life events such as marriage, buying a home, having a child, changing jobs, or starting a business.

Can one investment be used for multiple financial goals?

It can, but it’s usually better to assign different investments to different goals. This makes it easier to track progress and avoid withdrawing money meant for long-term goals too early.

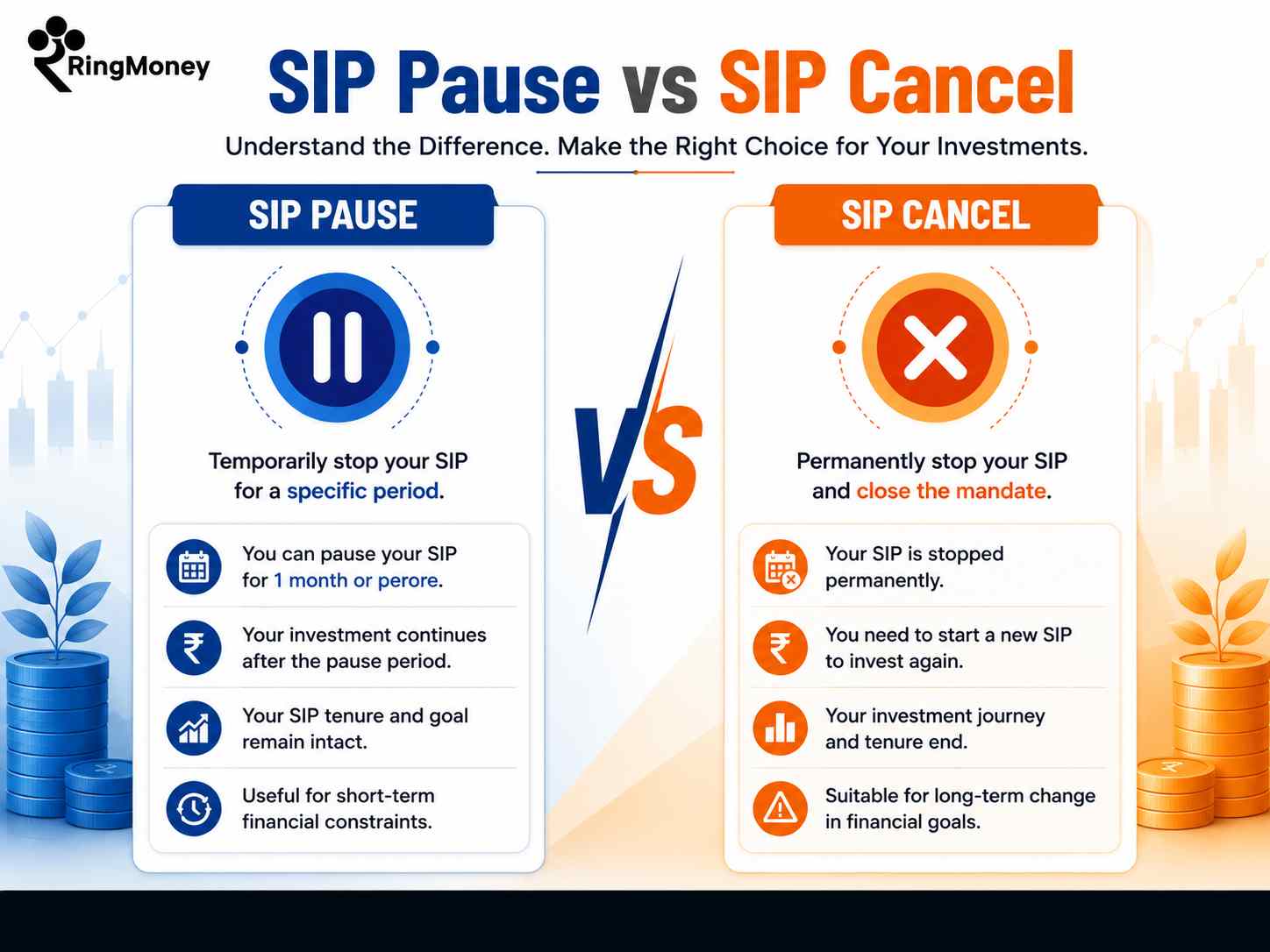

Should I stop my SIP if my goals change?

Not always. Sometimes you only need to increase, decrease, or redirect your SIP towards a different goal rather than stopping it completely.

What if I'm not sure what my investments were originally meant for?

That’s a good reason to review your portfolio. Start by identifying your current financial goals, then check whether each investment still supports one of them. If it doesn’t, it may be time to reconsider its role.