If your goal is purely wealth creation, a long-term SIP will usually generate more wealth than buying a residential flat. Higher compounding potential, lower ownership costs, and greater liquidity give equity mutual funds a clear mathematical edge in most scenarios.

Yet millions of Indians still prioritise buying a home before investing seriously. That’s because a house offers something an SIP never can: stability, security, and a sense of ownership.

Imagine two friends starting with the same ₹15 lakh and the same monthly budget of ₹50,000. One chooses a home loan, the other chooses rent and SIPs. Twenty years later, their wealth outcomes may be far more different than most people expect.

The real question is whether owning a flat is the best way to grow your money, or simply the most emotional financial decision most Indians make.

To answer that, let’s compare where the same money goes in both cases and what it could be worth 20 years later.

Why Most Indians Confuse Asset Ownership With Wealth Creation

The belief that buying a home automatically makes you wealthier is deeply rooted in Indian culture. For decades, property ownership was seen as protection against uncertainty, with parents encouraging their children to buy homes as early as possible. Renting, meanwhile, was often viewed as “money going down the drain.”

But there is an important distinction many people overlook.

A home can be both:

- A place to live

- An investment asset

The problem begins when these two roles get mixed.

Your primary residence provides utility. It gives you shelter, stability, and emotional comfort. Those benefits are real and valuable. However, an asset creates wealth only when its long-term growth meaningfully exceeds the costs of owning it.

This distinction matters because many homeowners focus only on rising property values while overlooking factors such as loan interest, maintenance expenses, taxes, and opportunity costs. These costs may not be visible on a property brochure, but they directly affect the wealth you ultimately create.

Ultimately, wealth creation is not determined by what you own. It is determined by what remains after all costs have been deducted.

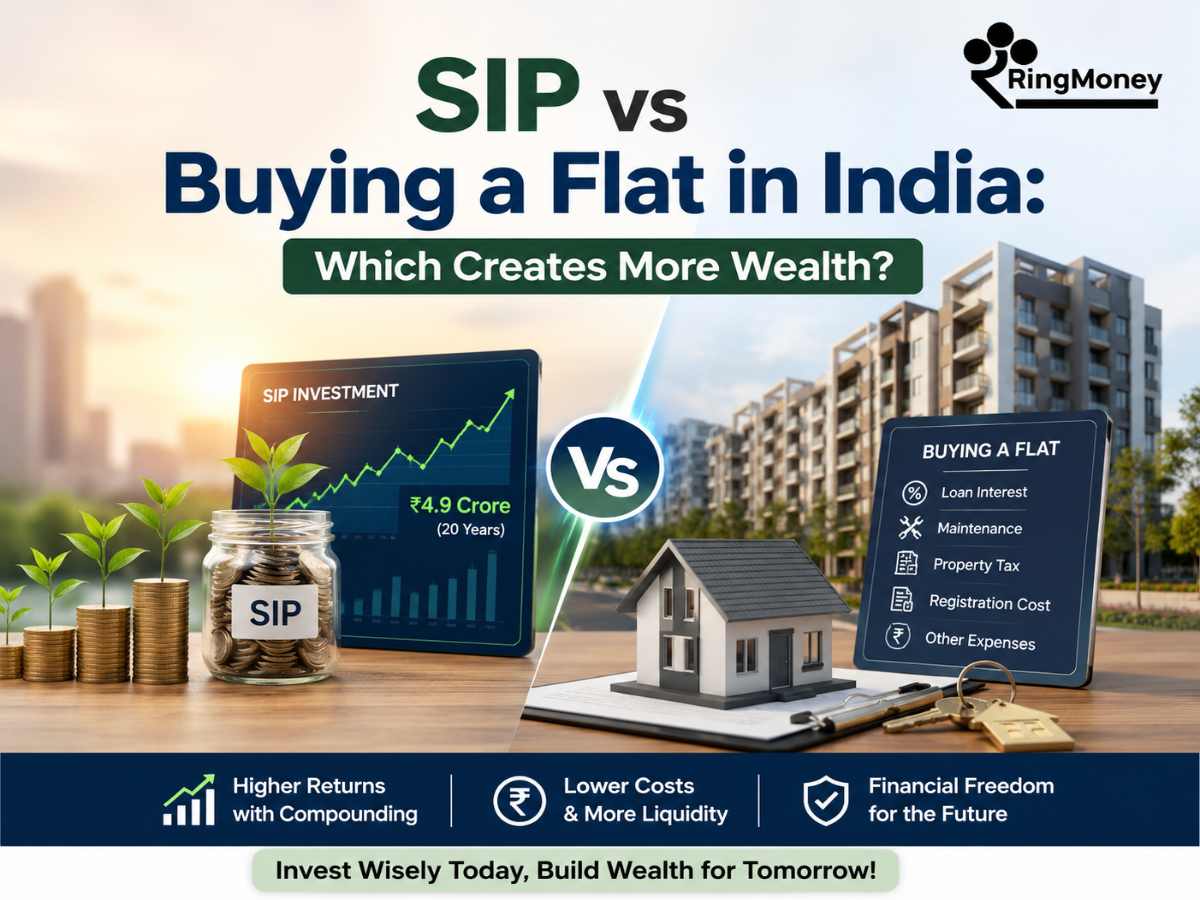

Tracking the Same Monthly Budget of ₹50,000

To make this comparison fair, let’s assume the same amount leaves your bank account every month.

Path | Monthly Outflow | Purpose |

Homebuyer | ₹50,000 EMI | Home loan repayment |

Investor | ₹15,000 Rent + ₹35,000 SIP | Housing + wealth creation |

At first glance, the homeowner appears to be building an asset while the renter is simply paying rent.

But that view ignores where the remaining money goes.

The renter-investor is not spending ₹50,000 and receiving nothing in return. A significant portion is being redirected into an investment vehicle that compounds over time.

![]()

This is where the comparison becomes interesting.

The Silent Wealth Machine Most People Underestimate

The biggest advantage of SIP investing is not higher returns. It is compounding.

Historically, diversified Indian equity mutual funds have delivered approximately 12% to 14% annualized returns over long periods, although future returns are never guaranteed. Residential property appreciation across many Tier-1 Indian cities has generally ranged between 5% and 7% CAGR over extended periods.

That difference may seem small. It is not. A few percentage points sustained over decades can create an enormous wealth gap.

Consider a simple example. A monthly SIP of ₹35,000 invested for 20 years at 12% annual growth could potentially grow to approximately ₹3.5 crore. At 14%, the corpus can move substantially higher.

The reason is simple: every year’s gains begin generating their own gains. That is the mathematical force behind compounding. Many investors underestimate it because they focus on monthly contributions rather than long-term accumulation.

The Hidden Expenses That Quietly Eat Your Returns

One of the biggest mistakes property investors make is calculating returns using only the purchase price and the selling price.

Real estate ownership involves numerous costs that rarely appear in marketing brochures.

Some of the most significant expenses include:

- Stamp duty and registration charges are paid upfront

- Brokerage fees during purchase and sale

- Property taxes are paid periodically

- Society maintenance charges that increase over time

- Major repairs and renovations

- Sinking fund contributions

- Home insurance costs

- Loan processing charges

For an ₹80 lakh property, these expenses can collectively amount to several lakhs over the holding period.

Unlike investment returns, these costs do not compound in your favour. They quietly reduce your actual profitability. This is why headline property appreciation figures often paint an incomplete picture.

Are You Building Equity—or Paying Interest for 20 Years?

Many first-time homebuyers are surprised when they learn how a home loan actually works. A typical Indian home loan follows an amortisation structure, where, in the early years, most of your EMI goes toward interest rather than principal repayment.

In practical terms, this means that during the first five to seven years:

- A large share of your EMI pays the bank’s interest

- A relatively small portion reduces your loan balance

- Equity accumulation happens slowly

This creates what many financial planners call the “front-loaded interest problem.”

You may feel like you are aggressively building ownership every month. In reality, you are initially paying a significant amount for the privilege of borrowing money. Understanding this structure is crucial because many property return calculations ignore how much interest is paid throughout the loan tenure.

When Life Hits Hard, Which Investment Actually Shows Up?

Every financial plan looks great until life becomes unpredictable. Job losses happen. Medical emergencies happen. Unexpected business opportunities appear.

This is where liquidity becomes important.

A mutual fund portfolio can usually be partially redeemed within a few working days. You can withdraw exactly the amount required while leaving the rest invested.

Real estate works differently. You cannot sell one room of your apartment. You cannot liquidate 15% of your property to fund a medical emergency. Selling a flat can take months depending on market conditions, location, and buyer availability. Sometimes sellers are forced to accept lower prices simply because they need cash quickly.

Liquidity may not seem important today. It becomes extremely important when circumstances change.

A financial asset is not just defined by how much it grows. It is also defined by how quickly it can help you when you need it most.

Can Your Flat Pay You Like a Business?

Many people justify property purchases by pointing to rental income. The assumption sounds logical: buy a property, collect rent, and build passive income.

The reality is often less attractive.

Residential rental yields in India typically remain around 2% to 3% annually. This means an ₹80 lakh property may generate only ₹1.6 lakh to ₹2.4 lakh per year in gross rental income.

Now compare that with home loan costs, which frequently range between 8.5% and 9.5%. This creates a significant negative spread.

In simple terms:

- Borrowing costs remain high

- Rental income remains relatively low

- The investment relies heavily on future appreciation

This does not mean property cannot generate profits. It means rental income alone is often insufficient to justify the economics.

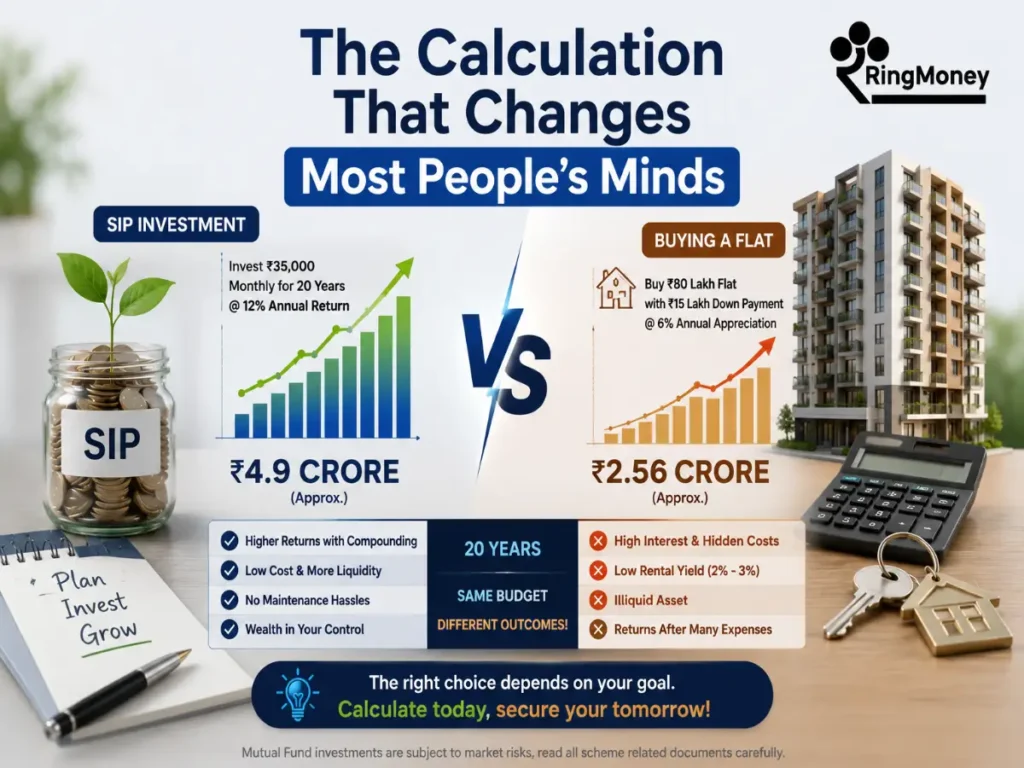

The Calculation That Changes Most People's Minds

Let’s compare a realistic 20-year scenario.

Scenario A: Buying the Flat

- Property Value: ₹80 lakh

- Down Payment: ₹15 lakh

- Home Loan: ₹65 lakh

- EMI: Approximately ₹50,000+

- Holding Period: 20 years

Assuming 6% annual appreciation, the property could be worth around ₹2.56 crore after 20 years.

Sounds impressive.

But remember, the final return is affected by several ownership costs, including:

- Interest paid to the bank

- Stamp duty

- Registration charges

- Maintenance expenses

- Property taxes

- Repair costs

All of these reduce actual wealth creation.

Scenario B: Rent + SIP

- ₹15 lakh invested immediately

- ₹35,000 monthly SIP

- ₹15,000 monthly rent

Assuming a long-term equity return of 12%, the ₹15 lakh lump sum alone could potentially grow to nearly ₹1.45 crore over 20 years. At the same time, a ₹35,000 monthly SIP could potentially build a corpus of around ₹3.5 crore.

Combined, the investment value can exceed ₹4.9 crore over the same period.

This highlights an often-overlooked opportunity cost: every rupee used as a down payment is a rupee that loses the chance to compound for the next two decades.

A common criticism of this strategy is that rent rises over time. That is true. In most cities, rents tend to increase by around 5% to 8% annually.

However, salaries also tend to rise over a 20-year career. For many professionals, income growth often outpaces rent growth, which means housing costs may consume a smaller percentage of income over time even as rent increases.

Property owners face a different challenge. Rental income rarely keeps pace with the total cost of ownership. Residential rental yields in India typically remain around 2% to 3%, while maintenance expenses, property taxes, society charges, and financing costs continue to rise. As a result, increasing rent alone is often not enough to meaningfully improve overall returns.

Even after accounting for rising rents, the wealth gap between a disciplined SIP strategy and a residential property investment often remains substantial.

The exact numbers will vary. But the underlying principle rarely changes: compounding tends to reward capital-efficient investments more than capital-intensive ones.

The Post-2024 Tax Reality Most Comparisons Ignore

Many older articles discussing real estate versus mutual funds are now outdated because recent tax changes have significantly altered the landscape.

One major development is that long-term capital gains taxation has become more aligned across asset classes. However, properties purchased after the July 2024 changes no longer enjoy the traditional indexation benefits that many investors relied upon.

This matters because indexation previously helped reduce taxable gains by adjusting purchase costs for inflation. Without it, long-term real estate returns may look less attractive than they did under earlier tax regimes.

Whenever you compare investment options, make sure you are using current tax rules rather than relying on outdated assumptions.

The Situations Where Buying a Flat Actually Makes More Sense

Despite everything discussed so far, buying a home is not a bad decision. In many situations, it may be the right decision.

- You Want Permanent Housing Stability

If moving every few years feels exhausting, ownership provides predictability and control.

- You Are Approaching Retirement

Retirees benefit from having housing costs largely eliminated through a debt-free home.

- You Struggle With Investment Discipline

Many investors stop SIPs during market corrections. A home loan acts as a forced savings mechanism.

- You Found an Exceptional Growth Location

Certain micro-markets experience significant infrastructure-led appreciation. These opportunities can outperform averages.

- Emotional Security Matters Deeply To You

Not every decision needs to be optimised for maximum return. Personal comfort has value.

Your Home Can Give Something SIPs Never Will

This is the part many financial debates ignore. A home delivers emotional returns. An SIP does not.

Your home can provide:

- A sense of permanence

- Stability for your family

- Freedom to renovate and customise

- Protection from landlord uncertainty

- Emotional comfort during uncertain times

These benefits cannot be measured through CAGR calculations. A mutual fund statement may show a larger number. But numbers alone do not determine the quality of life.

This is why the best financial decisions often balance both mathematical and emotional outcomes.

Can an SIP Help You Buy a Home Faster?

The debate is not always SIP versus a home loan. In many cases, an SIP can actually support your homeownership goals.

For example, if you start investing early, the accumulated corpus can help fund a future down payment, reduce the loan amount you need to borrow, or even be used to make partial prepayments on your home loan later. A smaller loan means lower interest costs and faster debt repayment.

Instead of viewing SIPs and homeownership as competing choices, many investors use SIPs as a tool to make buying a home more affordable.

So, What Creates More Wealth in India?

For most investors, the numbers favour SIPs. For most families, a home offers something numbers cannot: stability and peace of mind.

Ultimately, the right choice depends on your goal. If you’re optimising for maximum wealth, SIPs often come out ahead. If you’re optimising for long-term security and homeownership, buying a house may be worth the trade-off.

The real question is not whether a flat is better than an SIP. It’s whether you’re buying a home for financial returns, lifestyle needs, or a mix of both.