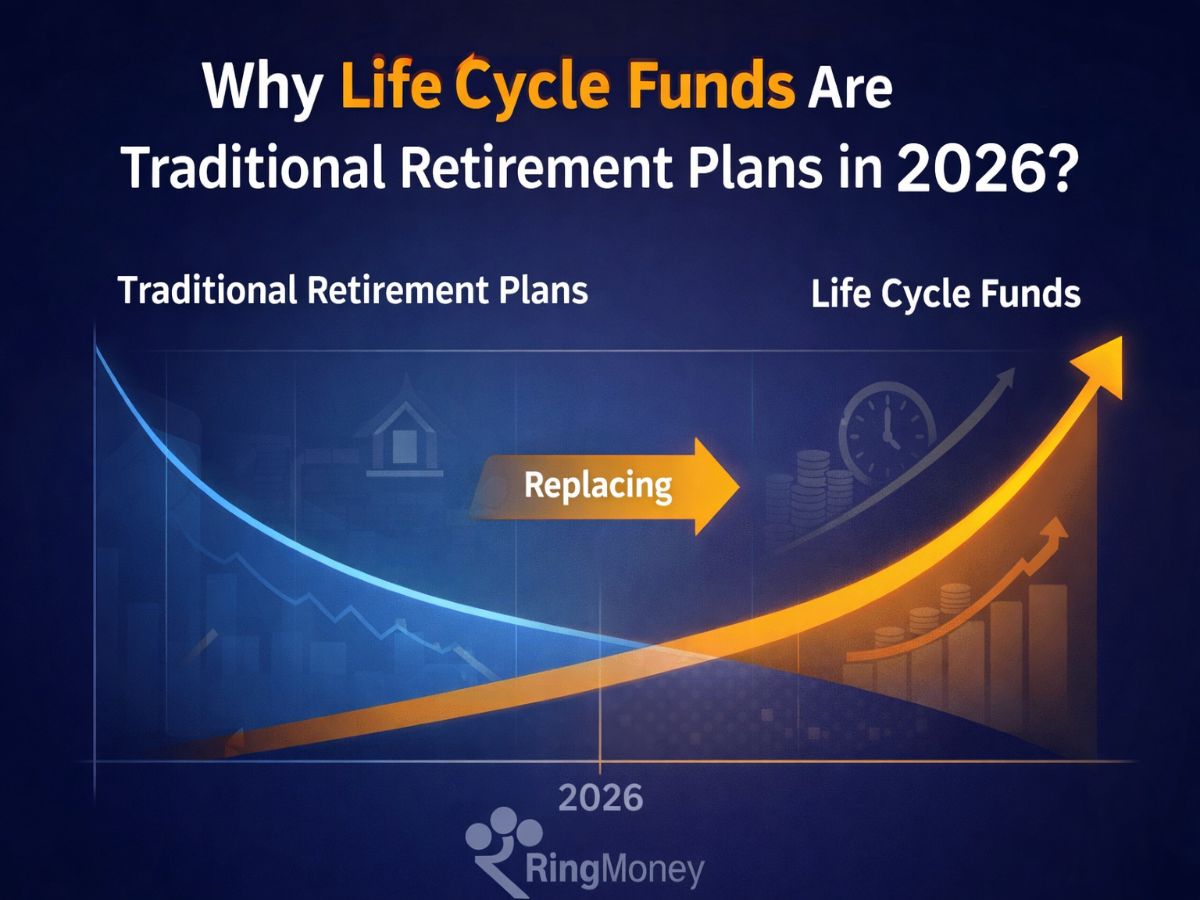

Why Life Cycle Funds Are Replacing Traditional Retirement Plans in 2026?

Retirement planning in India has entered a new era in 2026. Traditional retirement funds are being replaced by Life Cycle Funds because regulators want retirement investing to follow a clear, automated path that gradually reduces risk as investors approach their retirement year. Instead of relying on loosely structured “solution-oriented” schemes, the new framework ensures portfolios automatically shift from growth-focused equity to safer assets over time.

For years, many retirement funds promised long-term growth but lacked a disciplined structure for managing risk as retirement neared. The Securities and Exchange Board of India (SEBI) has now addressed this gap by introducing Life Cycle Funds — a maturity-based investment framework designed for goal-driven investing.

At RingMoney, we see this transition not just as a regulatory change but as an opportunity for investors to build smarter retirement plans through automated SIP investing, structured asset allocation, and long-term financial discipline.

The 2026 Retirement Shift: What Exactly Has Changed?

Traditional retirement funds were often marketed as long-term solutions, but the underlying asset allocation was largely defined by the fund house. That meant two retirement funds with similar goals could carry very different equity exposure and risk levels.

Life Cycle Funds solve this problem by introducing a target-year structure and a rule-based investment path.

Instead of manually adjusting your portfolio over decades, the fund automatically transitions from growth-focused assets to safer investments as retirement approaches.

In practical terms, this means investors no longer need to constantly rebalance between equity and debt funds themselves.

At RingMoney, we built our retirement investment experience around this new structure so investors can simply choose their retirement year and start investing through SIP while the glide path does the heavy lifting.

The Safety Floor: High-Quality Debt Protection

Another important safeguard in the 2026 Life Cycle framework focuses on credit quality in the final years before retirement.

For funds with less than 5 years to maturity, regulations require the debt portion to be invested in AA+ rated instruments or higher. This ensures the portfolio shifts toward high-quality and more stable debt assets as retirement approaches.

Why this matters:

- Higher credit quality: Debt investments move to AA+ or better rated instruments.

- Lower default risk: The portfolio becomes more defensive in the final years.

- Capital protection: The focus shifts from growth to preserving accumulated wealth.

For investors using RingMoney, this creates an additional layer of security. As your retirement timeline approaches, your portfolio doesn’t just reduce equity exposure — it transitions into high-quality debt designed to protect your savings.

Retirement Funds vs Life Cycle Funds: The Big Difference

The transition becomes clearer when we compare the old retirement fund structure with the new Life Cycle Fund framework.

Feature | Traditional Retirement Funds | Life Cycle Funds (2026 Framework) |

Regulatory category | Solution-oriented schemes | Dedicated Life Cycle Fund category |

Investment design | Fund house defined | SEBI-prescribed allocation bands |

Risk reduction | Not standardized | Automated glide path |

Maturity structure | No clear target year | Target maturity (5-year increments) |

Liquidity | 5-year lock-in common | Open-ended with exit loads |

Portfolio rebalancing | Often manual | Automatically managed |

The shift moves retirement investing from a label-based product to a goal-driven investment structure.

And this is exactly where RingMoney becomes valuable. Our platform helps investors easily match their retirement year with the right Life Cycle strategy and build a SIP plan that aligns with their timeline.

Understanding the “Glide Path”: The Core Idea Behind Life Cycle Funds

One of the biggest advantages of Life Cycle Funds is the automated glide path.

In simple terms, the investment strategy evolves as time passes.

When you are younger and retirement is far away, the portfolio holds a higher allocation to equity to capture growth. As the maturity year approaches, the fund gradually shifts toward debt and safer instruments.

For example:

Years Left to Retirement | Equity Allocation Range |

15–30 years | 65% – 95% |

10–15 years | 50% – 65% |

5–10 years | 35% – 50% |

Less than 1 year | 5% – 20% |

This structure allows investors to pursue long-term growth early on while reducing exposure to market volatility closer to retirement.

At RingMoney, we simplify this entire process. Instead of figuring out asset allocation manually every few years, investors can simply start a retirement SIP and let the Life Cycle structure manage the transitions.

The Inflation Shield: Gold and Silver Inclusion

Most traditional retirement plans relied heavily on just two assets — equity and debt. The 2026 Life Cycle Fund framework expands this structure by allowing limited exposure to additional assets that can strengthen long-term portfolio stability.

Under the new rules, Life Cycle Funds can allocate up to 10% of the portfolio to gold, silver, and certain infrastructure assets such as InvITs. This creates a more balanced portfolio that can potentially act as a hedge during periods of inflation or currency volatility.

For investors using RingMoney, this means your retirement strategy is no longer confined to a simple stock-bond mix. The Life Cycle approach can incorporate multiple asset classes within the same fund, helping protect the real value of your savings while still pursuing long-term growth through disciplined SIP investing.

Why Investors Are Moving Away from Traditional Retirement Plans

The shift to Life Cycle Funds did not happen randomly. It addresses several long-standing challenges investors face with older retirement schemes.

- Lack of Consistency

Traditional retirement funds often carried different risk profiles even when they targeted the same retirement goal. This made outcomes unpredictable for investors.

Life Cycle Funds bring standardised allocation bands, creating a more disciplined investment journey.

- No Clear Risk Transition

Older funds did not always reduce equity exposure systematically as retirement approached.

Life Cycle Funds enforce a structured risk-reduction pathway, protecting accumulated wealth over time.

- Liquidity and Flexibility

Many retirement schemes had rigid lock-in periods.

The new framework replaces strict lock-ins with an exit load structure:

- 3% exit load within the first year

- 2% exit load within the second year

- 1% exit load within the third year

This approach discourages short-term withdrawals while still allowing flexibility.

RingMoney users can track their investment timeline and exit load period clearly through the app dashboard, helping them stay invested with confidence.

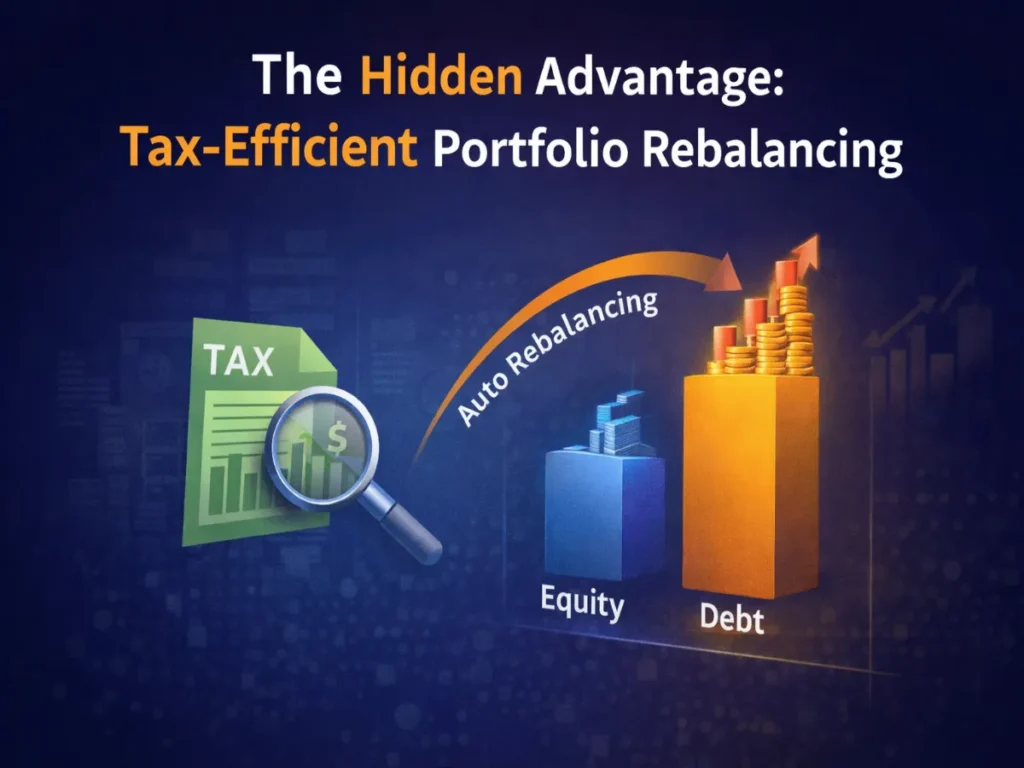

The Hidden Advantage: Tax-Efficient Portfolio Rebalancing

One of the most overlooked benefits of Life Cycle Funds is tax efficiency.

When investors manually rebalance portfolios by switching between equity and debt funds, those transactions may trigger capital gains tax.

Life Cycle Funds avoid this problem because rebalancing happens within the fund itself.

This allows investors to keep more of their returns compounding instead of paying taxes during the transition.

At RingMoney, we prioritise retirement strategies that maximise long-term compounding, which is why Life Cycle Funds are becoming a central part of our retirement planning experience.

Why SIP Is the Smartest Way to Invest in Life Cycle Funds

A Life Cycle Fund works best when combined with Systematic Investment Plans (SIPs).

Instead of investing a lump sum, SIPs allow investors to contribute regularly, building their retirement corpus steadily over decades.

Through RingMoney, investors can start a retirement SIP in minutes and benefit from:

- disciplined long-term investing

- rupee cost averaging

- automated portfolio growth

- gradual risk reduction through the glide path

The combination of SIP discipline and Life Cycle structure creates a powerful retirement planning framework.

Why RingMoney Is the Best App for Retirement Planning in 2026

Many investors understand the importance of retirement planning but struggle with execution. Choosing the right fund, monitoring allocations, and maintaining discipline can be complicated.

RingMoney removes that complexity.

We built our platform to make retirement investing simple, structured, and transparent.

Here is what makes RingMoney the preferred retirement planning app for modern investors:

Personalised Retirement Targeting

Our system helps investors choose Life Cycle strategies based on their expected retirement year, ensuring investments align with long-term goals.

Simple SIP Setup

Starting a retirement SIP on RingMoney takes only a few steps. Investors can automate contributions and focus on consistency rather than constant portfolio adjustments.

Intelligent Portfolio Visibility

Users can track how their investments evolve, including the glide path transition from equity to safer assets.

The Future of Retirement Investing Has Already Begun

The 2026 regulatory shift marks a clear evolution in how retirement investing works in India.

Traditional retirement funds relied heavily on labels and fund manager discretion. Life Cycle Funds introduce a structured, transparent path that aligns investments with long-term goals.

For investors, this means:

- clearer retirement planning

- automatic risk management

- better tax efficiency

- improved flexibility

At RingMoney, we designed our platform to make this transition seamless.

Instead of worrying about portfolio adjustments every few years, investors can simply choose their retirement horizon, start a SIP, and allow the Life Cycle strategy to guide the journey.

Start Your Retirement Plan with RingMoney Today

Retirement is one of the most important financial goals in life, yet many investors delay planning because the process feels complicated.

The new Life Cycle framework removes that complexity, and RingMoney makes it even easier.

With our platform, you can build a structured retirement plan, automate SIP investments, and benefit from a disciplined glide path designed for long-term financial security.

The rules of retirement investing have changed in 2026.

Now is the time to adapt.

Download the RingMoney app today and start building a smarter, automated retirement plan that grows with you for the decades ahead.

For regular investment tips, SIP updates, and simple money guidance, follow us on Instagram and explore the link in our bio to get started instantly.