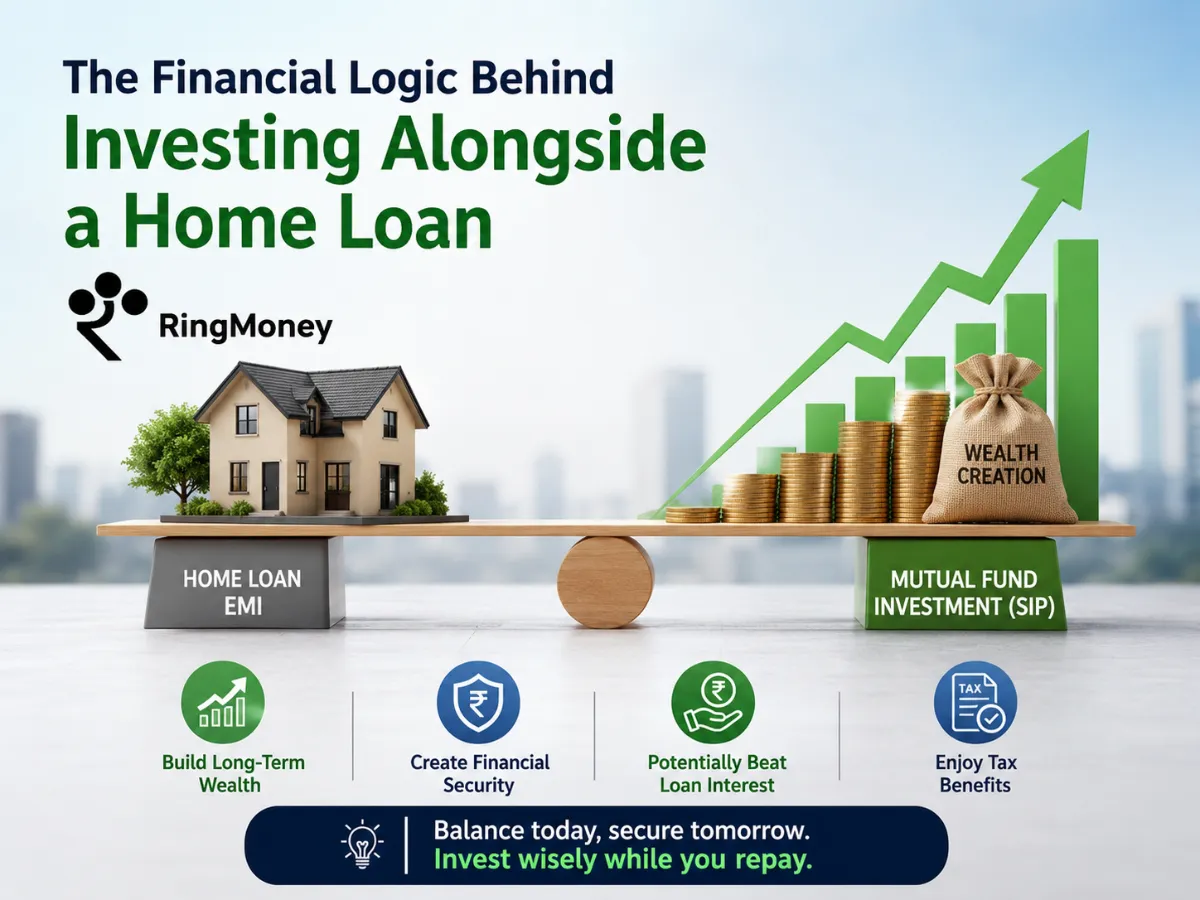

The core argument behind this strategy comes down to return potential.

If a borrower aggressively prepays a home loan carrying an effective interest cost of around 8%–9%, the savings are fixed and guaranteed. However, long-term diversified equity mutual funds have historically generated higher return potential over extended periods.

This does not mean mutual funds are risk-free. Markets fluctuate, and returns are never guaranteed. But over long investment horizons, equities have generally outperformed inflation and fixed borrowing costs.

For taxpayers claiming deductions under applicable home loan tax benefits, the effective post-tax loan cost may be reduced even further. In some cases, this makes investing mathematically more efficient than aggressive prepayment.

For salaried borrowers, home loans also come with tax advantages. Under Section 24(b) of the Income Tax Act, individuals can claim deductions of up to ₹2 lakh annually on home loan interest payments for a self-occupied property. This can reduce the effective cost of borrowing, which is one reason many investors prefer balancing EMIs with long-term mutual fund investments instead of aggressively prepaying the entire loan.

That said, the strategy only works when investments are disciplined and long-term.

Even the best investment strategy fails without consistency.

Managing EMIs, expenses, insurance, savings, and investments together can become overwhelming when platforms feel cluttered or complicated. Borrowers need simplicity because long-term investing works best when it becomes automatic.

This is where we believe RingMoney creates real value.

Instead of turning investing into a complex experience, we focus on making mutual fund investing straightforward, clean, and easy to manage alongside existing financial commitments like home loan EMIs. From starting SIPs to tracking progress over time, the platform is designed to help investors stay disciplined without unnecessary distractions.

For borrowers trying to maintain a long-term “SIP + EMI” strategy, simplicity often becomes the biggest advantage.