Redeeming mutual funds often feels like a simple financial action, but the real complexity starts when it reaches your Income Tax Return. Every redemption, whether it results in profit or loss, needs to be correctly reported under the appropriate schedule and section in your ITR form.

Most tax notices and mismatches do not come from non-payment of tax, but from incorrect classification under Schedule CG, Section 111A, or Section 112A. Once the structure is understood clearly, reporting becomes predictable and far less stressful.

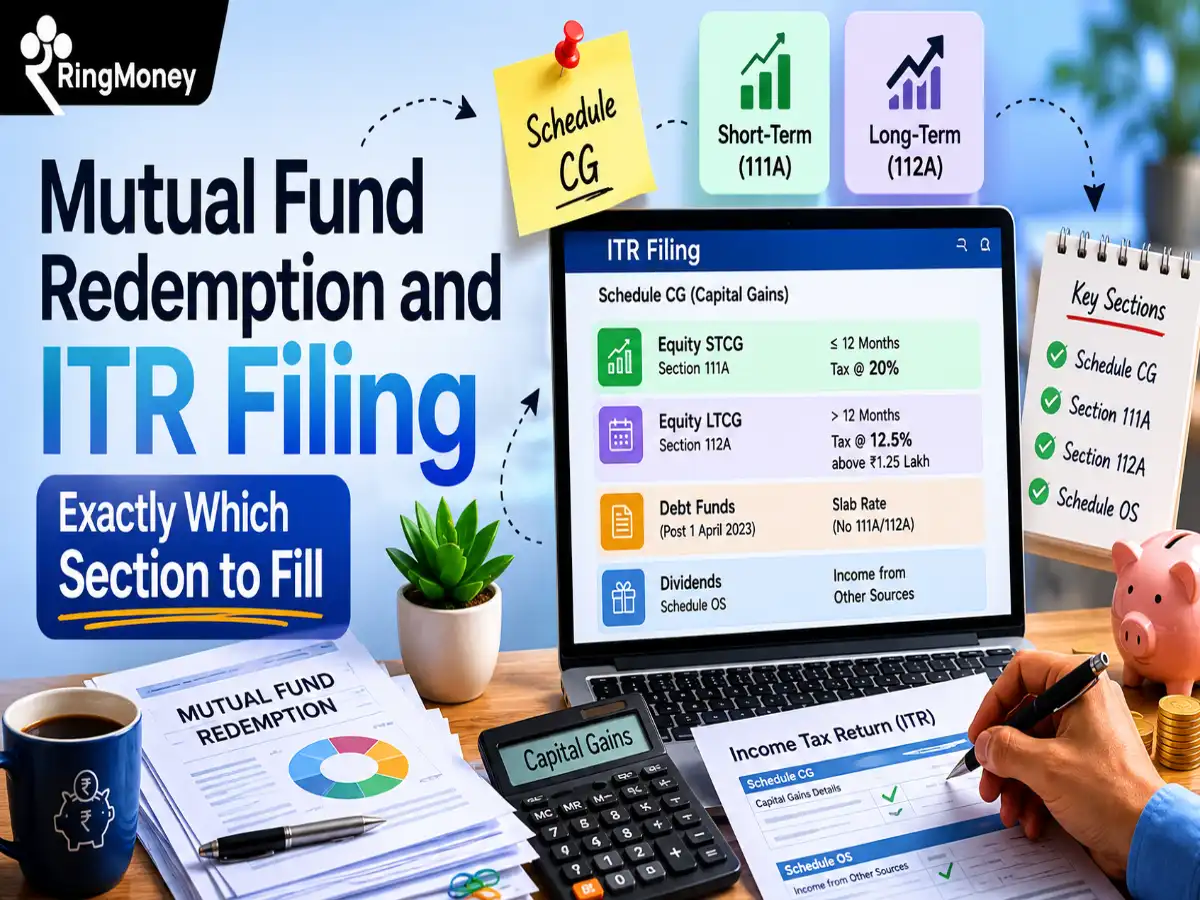

Mutual fund redemption must be reported in Schedule CG (Capital Gains) of your ITR. The exact section depends on the holding period and fund type.

- Section 111A (Schedule CG): For short-term equity mutual fund gains (held ≤ 12 months), taxed at 20%

- Section 112A (Schedule CG): For long-term equity mutual fund gains (held > 12 months), taxed at 12.5% above ₹1.25 lakh exemption

- Debt mutual funds (post 1 April 2023 purchases): Report under Schedule CG – normal income tax slab rates (no 111A/112A treatment)

- Dividends (if any): Report under Schedule OS (Income from Other Sources), not capital gains

That is the exact mapping required in the ITR filing.

Choosing the Right ITR Form for Mutual Fund Redemption

Before entering any numbers into your tax return, the first step is to identify the correct ITR form. This step is often overlooked, especially by salaried investors who assume ITR-1 is sufficient.

Once mutual fund units are redeemed, capital gains reporting becomes mandatory in most cases. That automatically changes the eligibility criteria for simplified forms.

Income Situation | Correct ITR Form | Applicability |

Salary + mutual fund capital gains | ITR-2 | Most salaried individuals |

Business or professional income + mutual funds | ITR-3 | Freelancers, traders, professionals |

Salary only, no capital gains | ITR-1 | Not valid if any mutual fund redemption exists |

The key understanding here is simple. The moment redemption occurs, the tax return must include capital gains schedules, which generally require filing ITR-2 or ITR-3.

Where Mutual Fund Redemption is Reported in ITR

All mutual fund redemption transactions are reported under Schedule CG (Capital Gains). This is the central section where the nature of gains determines how they are taxed and reported.

Within this schedule, classification depends on holding period and fund type. Equity, debt, and hybrid funds are treated differently under tax rules, and the correct section must be selected carefully.

Equity Mutual Funds and Their Tax Sections

Equity-oriented mutual funds include index funds, large-cap funds, flexi-cap schemes, and ELSS investments. Their taxation depends mainly on how long the units were held before redemption.

If units are sold within 12 months, the gains are considered short-term and reported under:

Section 111A in Schedule CG

These gains are taxed at 20%, and the reporting is relatively straightforward because consolidated figures are often sufficient.

If units are held for more than 12 months, the gains become long-term and must be reported under:

Section 112A in Schedule CG

Here, taxation becomes slightly more structured. Gains above ₹1.25 lakh in a financial year are taxed at 12.5%, while the exemption threshold is automatically applied during computation.

Debt Mutual Funds and Their Separate Tax Treatment

Debt mutual funds follow a different taxation structure, especially after recent regulatory changes. The holding period benefit has been significantly reduced for investments made after April 2023.

For debt funds purchased after 1 April 2023, all gains are treated as short-term regardless of holding duration. This means they are taxed at slab rates applicable to the individual.

These gains are still reported under Schedule CG, but they do not fall under Section 111A or 112A. Instead, they are included under normal income taxation rules.

This distinction is critical because incorrect classification of debt fund gains is one of the most common reasons for AIS mismatches and subsequent notices.

Mutual Fund Dividends and Where They Belong

Dividends from mutual funds are often mistakenly entered under capital gains, but they belong to a completely different schedule.

Dividend income must be reported under:

Schedule OS (Income from Other Sources)

These are taxed according to the individual’s income tax slab rate. In many cases, TDS is already deducted by the fund house when dividend payouts cross certain thresholds.

Keeping dividends separate from capital gains is essential for the correct computation and smooth processing of the return.

Detailed Requirements Under Section 112A

Long-term capital gains from equity mutual funds require detailed transaction-level reporting. Unlike short-term gains, where consolidated figures may be sufficient, long-term gains demand precision.

The Income Tax Department requires the following details for each transaction:

- ISIN (International Securities Identification Number) of the mutual fund

- Number of units redeemed

- Purchase price per unit

- Sale price per unit

- Exact purchase and redemption dates

This structured reporting ensures accurate tax calculation and helps match returns with government-reported AIS data.

Understanding AIS and CAS Reconciliation

One of the most overlooked aspects of mutual fund taxation is data reconciliation. The Income Tax Department now auto-populates mutual fund transactions in the Annual Information Statement (AIS), which is sourced directly from RTAs such as CAMS and KFintech.

Alongside AIS, investors also receive Consolidated Account Statements (CAS), which contain detailed fund-level data including NAV, units, and transaction history.

If there is even a minor mismatch between AIS and CAS, the return may be flagged for review. This makes reconciliation not just a best practice, but a necessity for accurate filing.

Step-by-Step Flow Inside the ITR Portal (Mutual Fund Redemption Reporting)

Step 1: Select the Correct ITR Form

Choose ITR-2 if you are a salaried individual with mutual fund capital gains, or ITR-3 if you have business/professional income. Do not use ITR-1 if any mutual fund redemption has taken place.

Step 2: Open Schedule CG (Capital Gains Section)

Navigate inside the ITR utility to “Income Details” → “Schedule CG”. This is where all mutual fund redemptions must be reported.

Step 3: Report Short-Term Equity Gains (Section 111A)

If equity mutual funds were sold within 12 months, enter them under Section 111A. These gains are taxed at 20%, where entering consolidated transaction totals is sufficient.

Step 4: Report Long-Term Equity Gains (Section 112A)

If equity mutual funds were held for more than 12 months, enter details under Section 112A. You must provide transaction-level details, including ISIN, units sold, purchase price, and sale price.

Long-term gains above the combined annual exemption limit of ₹1.25 lakh across all equity investments are taxed at 12.5%.

Step 5: Enter Debt Mutual Fund Gains

For debt mutual funds (especially those purchased after 1 April 2023), report gains under the normal income sections within Schedule CG. These are taxed at your applicable slab rate and do not fall under 111A or 112A.

Step 6: Use Schedule SI for Special Rate Income

Go to Schedule SI (Special Income) to ensure income taxed under Section 111A and Section 112A is correctly reflected for final tax computation.

Step 7: Add Dividend Income Separately

Report any mutual fund dividends under Schedule OS (Income from Other Sources). This should not be mixed with capital gains entries.

Step 8: Validate and Submit Return

Review all schedules carefully, cross-check AIS/CAS data, and proceed with validation, submission, and e-verification of the ITR.

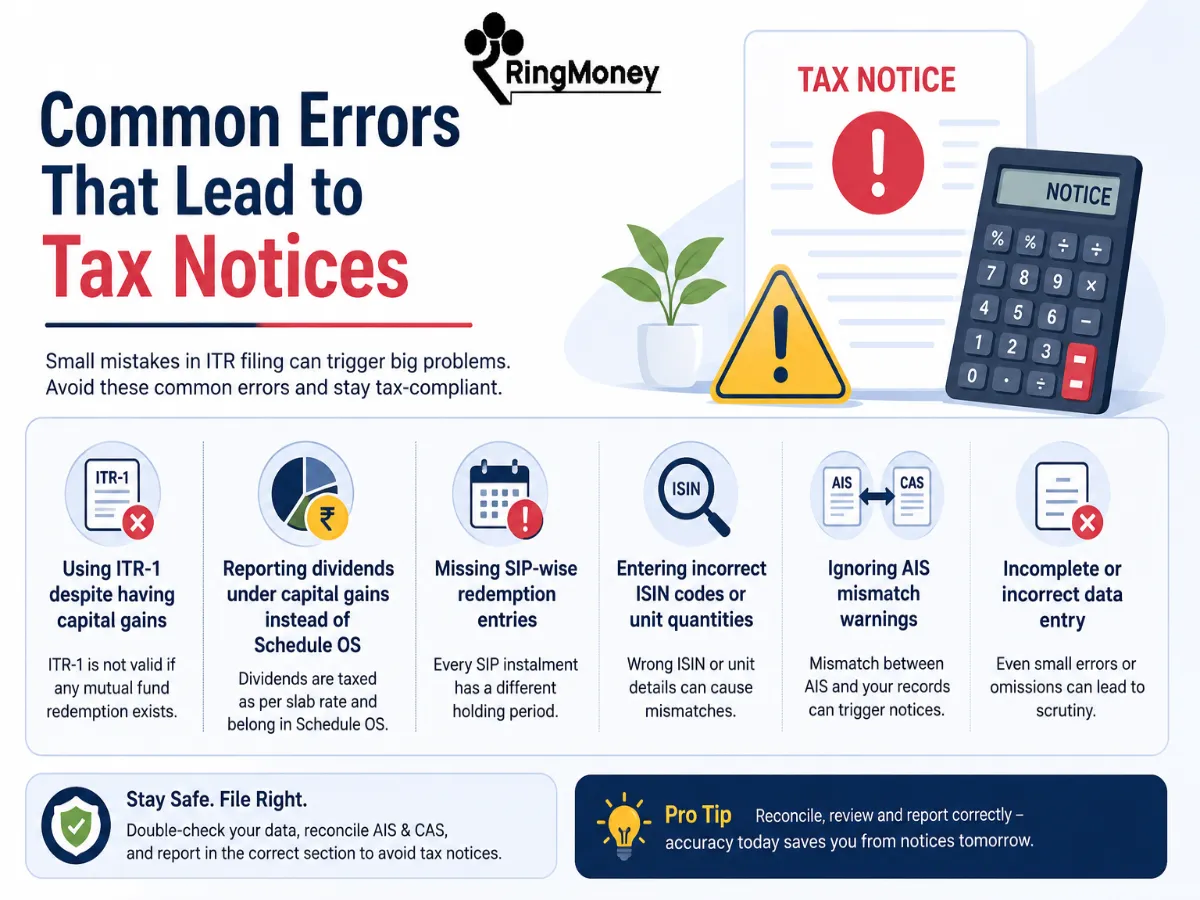

Common Errors That Lead to Tax Notices

Many tax notices are not caused by underreporting, but by incorrect categorisation or incomplete data entry. Understanding these mistakes helps prevent unnecessary complications.

Some of the most frequent issues include:

- Using ITR-1 despite having capital gains

- Reporting dividends under capital gains instead of Schedule OS

- Missing SIP-wise redemption entries

- Entering incorrect ISIN codes or unit quantities

- Ignoring AIS mismatch warnings during filing

Even small inconsistencies between reported and government-recorded data can trigger automated scrutiny.

Practical Tax Optimisation Insights

Beyond compliance, mutual fund taxation also offers opportunities for smarter planning. Loss adjustment rules, for example, allow investors to reduce taxable gains legally.

Short-term losses can be adjusted against both short-term and long-term gains, while long-term losses can only be adjusted against long-term gains. Any unused losses can be carried forward to future financial years.

Timing also plays an important role. Spreading redemptions across different financial years can help optimize the ₹1.25 lakh LTCG exemption threshold and reduce overall tax liability.

Why Organised Tracking Changes Everything

The biggest challenge in mutual fund taxation is rarely the tax rules themselves. The real problem begins when investors try to track SIPs, redemption dates, holding periods, and capital gains across multiple apps, AMC portals, emails, and statements during the ITR filing season.

This is exactly where RingMoney changes the experience completely. Instead of manually collecting CAS reports and reconciling transactions one by one, investors can manage their entire mutual fund journey in a single, organised ecosystem built for simplicity and accuracy.

With RingMoney, portfolio tracking becomes structured from day one. Investors can easily monitor redemption history, calculate holding periods correctly, access organised capital gains summaries, and keep investment records ready for tax filing without last-minute confusion.

More importantly, RingMoney helps reduce the chances of AIS mismatches, incorrect reporting, and manual filing errors that often lead to unnecessary notices. Rather than treating tax filing as a yearly struggle, we make investment tracking and ITR preparation far more seamless, reliable, and investor-friendly throughout the year.

Final Understanding of Mutual Fund ITR Reporting

Mutual fund taxation becomes straightforward once broken into three clear parts: classification of gains, correct schedule selection, and accurate data reconciliation with AIS.

The complexity usually arises not from tax laws themselves, but from fragmented financial data spread across multiple systems. Once that data is unified and properly tracked, filing becomes a structured exercise rather than a stressful reconstruction process.

A well-organised investment system, especially through platforms like RingMoney, ensures that investors spend less time decoding transactions and more time focusing on financial decisions that actually matter.

For regular investment tips, SIP updates, and simple money guidance, follow us on Instagram and explore the link in our bio to get started instantly.

Frequently Asked Questions

Can mutual fund losses also be reported in the ITR?

Yes, even losses should be reported in Schedule CG. Reporting losses allows investors to carry them forward and adjust against future capital gains.

Do SIP redemptions get taxed differently from lump sum investments?

No, but each SIP instalment is treated as a separate investment with its own holding period. Tax is calculated individually for every redeemed unit.

What happens if AIS and CAS values are different?

Minor mismatches can trigger scrutiny or notices from the Income Tax Department. Always reconcile AIS with your CAMS or KFintech statement before filing.

Is switching from one mutual fund scheme to another taxable?

Yes, even internal switches between schemes are treated as redemption and fresh purchase transactions, making them taxable events.

Can capital gains tax be reduced legally on mutual funds?

Yes, investors can use tax-loss harvesting, stagger redemptions across financial years, and utilise the ₹1.25 lakh LTCG exemption strategically to optimise taxes.