For years, ₹1 Crore has been one of the most popular SIP goals. It sounds like a big number, and for many investors, reaching it feels like achieving financial security.

But if you’re investing for a goal that’s 15, 20, or even 30 years away, there’s an important question to consider: will ₹1 Crore have the same value in the future that it has today?

As the cost of living rises over time, the purchasing power of your money falls. That means a ₹1 Crore corpus may not support the lifestyle, retirement, or financial freedom you expect years from now.

Reaching ₹1 Crore is still a great milestone. The challenge is making sure it’s enough for the future you’re planning for.

The ₹1 Crore Illusion Most Investors Fall For

When you invest through SIPs, your real goal isn’t to accumulate a number in your account. You’re investing to fund important life goals such as:

- A comfortable retirement

- Better healthcare

- Travel and experiences

- A secure lifestyle

- Protection against unexpected expenses

The problem is that many investors become focused on reaching ₹1 Crore and forget what that money is supposed to achieve.

A corpus is only a tool. What matters is whether it can support your future lifestyle. If living costs continue to rise, a ₹1 Crore corpus that looks impressive today may not feel nearly as large when you actually need it.

That’s why successful investing isn’t about chasing a milestone. It’s about building enough purchasing power to fund the life you want in the future.

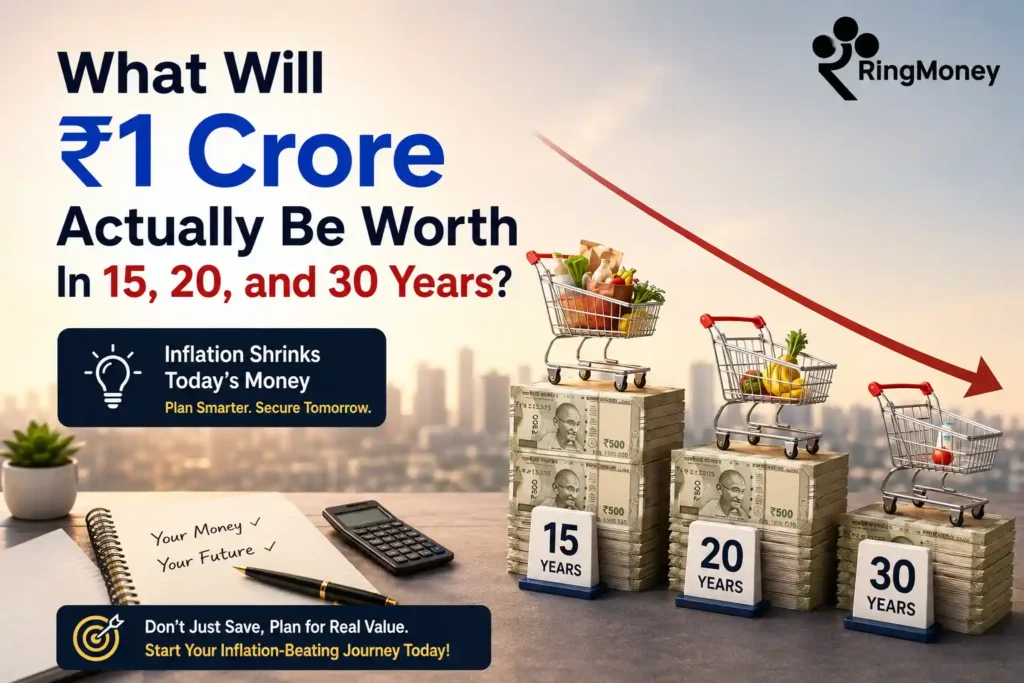

What Will ₹1 Crore Actually Be Worth In 15, 20, and 30 Years?

You don’t need a finance degree to understand inflation. Just think about how much things cost 15 or 20 years ago compared to today. A budget that once felt comfortable often feels inadequate now.

The same thing will happen to your future corpus. If inflation averages 6% a year, ₹1 Crore won’t have the same buying power when you finally reach it.

Years Later | Real Value of ₹1 Crore |

Today | ₹1 Crore |

15 Years | ~₹41.7 Lakh |

20 Years | ~₹31 Lakh |

30 Years | ~₹17.4 Lakh |

In other words, a ₹1 Crore corpus after 30 years could buy roughly what ₹17 lakh buys today. The number stays the same, but its purchasing power doesn’t.

The Inflation Most Investors Underestimate

There’s another catch. Your biggest future expenses—such as healthcare, education, housing, and insurance—often become more expensive faster than average inflation.

As your income grows, your lifestyle usually grows too. That’s why planning with only a basic inflation assumption can leave you underprepared. Your future costs may rise much faster than you expect.

Would You Retire on ₹17 Lakh?

Imagine your SIP finally reaches ₹1 Crore after 30 years. It’s a milestone worth celebrating, but then you look at the reality around you.

Healthcare costs are higher, daily expenses have increased, and the lifestyle you want in retirement costs far more than it does today. Suddenly, that ₹1 Crore doesn’t feel as large as it once did.

This isn’t because your investments underperformed. It’s because the target was never adjusted for inflation and future living costs.

Many investors focus on reaching a number when they should be focused on funding a future lifestyle. The biggest risk isn’t missing your goal—it’s reaching a goal that no longer supports the life you want.

The Silent Wealth Killer: Flat SIP Investing

Another mistake many investors make is treating their SIP as a one-time setup. They start with ₹10,000 or ₹15,000 per month and keep the amount unchanged for years.

The problem is that while your salary, expenses, and cost of living continue to rise, your SIP stays fixed.

Financial Variable | What Happens Over Time |

Salary | Increases |

Expenses | Increase |

Cost of Living | Increases |

SIP Amount | Remains Fixed |

This means you’re gradually saving a smaller portion of your income, even though you’re earning more. For example, if your salary grows by 8% every year but your SIP never changes, your investment effort effectively declines over time.

A fixed SIP can still build wealth, but it may not keep pace with your future financial needs.

Why the 15-15-15 Rule Tells Only Half the Story

The 15-15-15 rule is one of the most popular investing formulas. The idea is simple:

- Invest ₹15,000 per month

- Stay invested for 15 years

- Earn 15% annual returns

Remember, your long-term equity returns will also face Long-Term Capital Gains (LTCG) tax upon withdrawal, shrinking your actual take-home corpus even further.

Under these assumptions, you could build a corpus of around ₹1 Crore. It’s a great example of how powerful compounding can be.

The problem is that the rule focuses on reaching a number, not what that number will actually be worth in the future. It doesn’t account for factors such as inflation, taxes, rising living costs, or how much money you’ll need to maintain your lifestyle years from now.

There’s nothing wrong with the math behind the rule. The challenge is that a ₹1 Crore target may look very different 15 or 20 years from today than it does right now.

That’s why popular investing rules should be treated as useful guidelines, not complete financial plans.

Stop Targeting ₹1 Crore. Start Targeting Your Future Lifestyle

The best financial plans start with your future expenses, not a round number like ₹1 Crore.

Instead of asking, “How do I reach ₹1 Crore?”, ask, “How much money will I need to maintain the lifestyle I want?”

For example, if your household expenses are ₹50,000 a month today, they could exceed ₹2 lakh a month after 25 years if inflation averages around 6%. That means your retirement target may need to be much larger than you originally expected.

When you calculate your goals based on future expenses, you can:

- Set more realistic targets

- Account for inflation

- Estimate retirement needs more accurately

- Avoid under-saving

The key is simple: your future lifestyle should determine your investment target, not the other way around.

The One SIP Upgrade That Can Double Your Wealth

One of the simplest ways to keep up with inflation is through a Step-Up SIP. Instead of investing the same amount every year, you increase your SIP by 5% to 10% annually, ideally in line with your salary growth.

For example:

Year | Flat SIP | Step-Up SIP |

1 | ₹10,000 | ₹10,000 |

2 | ₹10,000 | ₹11,000 |

3 | ₹10,000 | ₹12,100 |

4 | ₹10,000 | ₹13,310 |

The increase may seem small at first. A 10% step-up on a ₹10,000 SIP is just ₹1,000 extra per month in the second year. But over 20 or 30 years, those gradual increases can significantly boost your final corpus because every additional investment gets more time to compound.

Flat SIP | Step-Up SIP |

Fixed investment | Growing investment |

Falls behind income growth | Grows with income |

Harder to beat inflation | Better positioned against inflation |

Lower long-term corpus | Higher long-term corpus |

The goal isn’t simply to invest more. It’s to make sure your investments grow as your income grows, so your future wealth keeps pace with your future needs.

Looking for an Easier Way to Start a Step-Up SIP?

A Step-Up SIP works best when the increase happens consistently every year. The challenge is that many investors forget to review their SIPs or postpone increasing their contributions, even after receiving salary hikes.

That’s where RingMoney can help.

With RingMoney, you can start your investment journey and build the habit of increasing your SIP over time, helping your investments grow alongside your income. Instead of relying on a fixed investment amount for years, you can take a more proactive approach to long-term wealth creation and stay better prepared for rising future costs.

If your goal is not just to reach a number but to build wealth that keeps pace with your future lifestyle, RingMoney can be a useful platform to support that journey.

A Better Formula for Building Inflation-Proof Wealth

Building meaningful long-term wealth requires a different framework. Instead of focusing solely on a headline number, consider these three principles.

1. Calculate Future Lifestyle Costs

Estimate what your desired lifestyle will cost years from now. Factor in:

- Housing

- Healthcare

- Daily living expenses

- Travel

- Education

- Emergency reserves

Future costs matter more than today’s costs.

2. Increase Your SIP Every Year

Whenever your income rises, increase your investments too. Even a modest annual top-up can create a significant difference over long investment horizons.

Automation makes this process easier and removes the temptation to delay.

3. Stay Invested Long Enough to Beat Inflation

Short-term market fluctuations matter far less than long-term compounding. Growth-oriented investments need time to generate returns that comfortably exceed inflation.

The longer your time horizon, the greater the opportunity to build real wealth rather than merely nominal wealth.

When ₹1 Crore Isn't the Finish Line

Reaching ₹1 Crore is a major milestone, but a milestone and a financial plan are not the same thing.

What matters isn’t the number in your portfolio—it’s the lifestyle that number can support. If your goals are still 20 or 30 years away, inflation, rising healthcare costs, and changing expenses can significantly reduce the value of that future corpus.

That’s why the smartest investors don’t target a round number. They target the future lifestyle they want to fund and build their investments around that goal.

Before setting ₹1 Crore as your SIP target, ask yourself one question: Will it be enough for the life you want when you actually need it?

Frequently Asked Questions

Is it better to invest a larger amount later or start a smaller SIP today?

Starting early is usually more powerful because compounding needs time to work. Even a smaller SIP started today can outperform a larger investment started several years later.

How often should you review your SIP goals?

A yearly review is usually enough. Reassess your goals whenever there’s a major life change such as marriage, a home purchase, the birth of a child, or a significant increase in income.

Should your emergency fund and SIP investments be separate?

Yes. An emergency fund is meant for short-term financial shocks, while SIPs are designed for long-term wealth creation. Mixing the two can force you to withdraw investments at the wrong time.

Can inflation ever be higher than your investment returns?

Yes. During certain periods, inflation can temporarily outpace investment returns. That’s why long-term investors often use growth-oriented assets like equity mutual funds to improve their chances of beating inflation over time.

What's a common mistake investors make besides keeping their SIP amount fixed?

Many investors stop investing during market downturns. However, market corrections often allow SIPs to buy more units at lower prices, which can benefit long-term returns when markets recover.