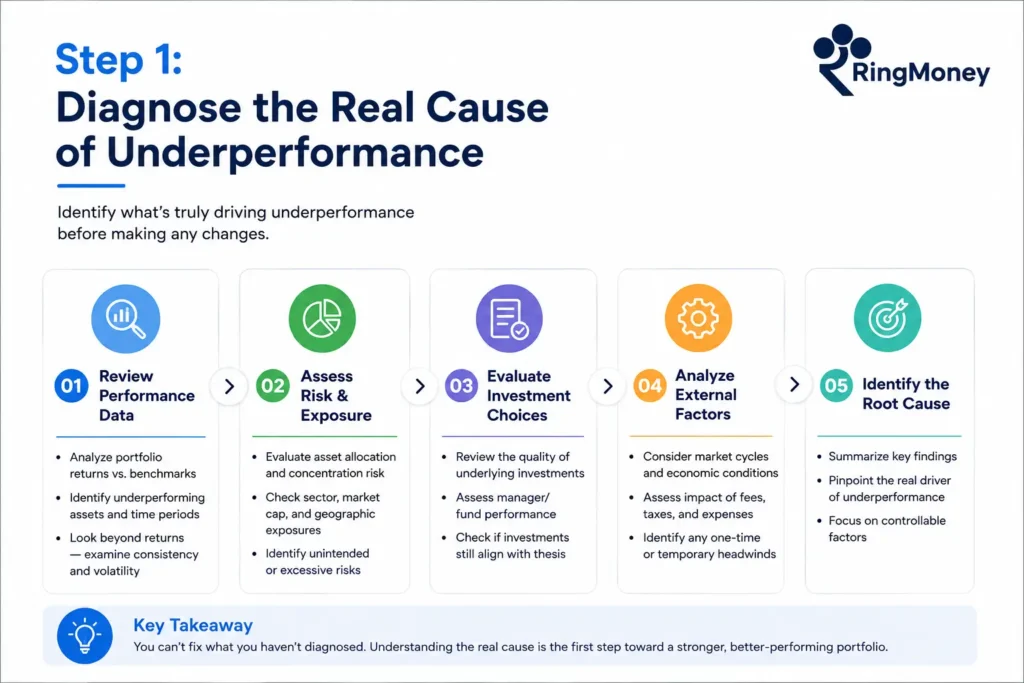

Most investors skip this step and jump straight to redemption. That usually locks in losses unnecessarily.

A proper diagnosis looks at three layers.

Benchmark comparison

Every mutual fund has a benchmark index. This is the first and most important reference point. If your fund consistently lags behind its benchmark across multiple market phases, it signals inefficiency in stock selection or strategy execution.

Short-term deviations don’t matter. Persistent gaps over time do.

Peer comparison within a category

Next, compare the fund with others in the same category. A mid-cap fund should be evaluated against other mid-cap funds, not across asset classes.

If most peers are performing better, the issue is likely fund-specific rather than market-driven.

Style cycles and sector behavior

Markets rotate between styles like growth, value, momentum, and quality. A fund can underperform simply because its strategy is temporarily out of favour.

For example, value-focused funds may lag during strong growth-driven rallies, but perform better over full cycles.

Sector funds add another layer of volatility. A banking or IT fund depends heavily on sector health, so underperformance may reflect industry conditions rather than fund management.

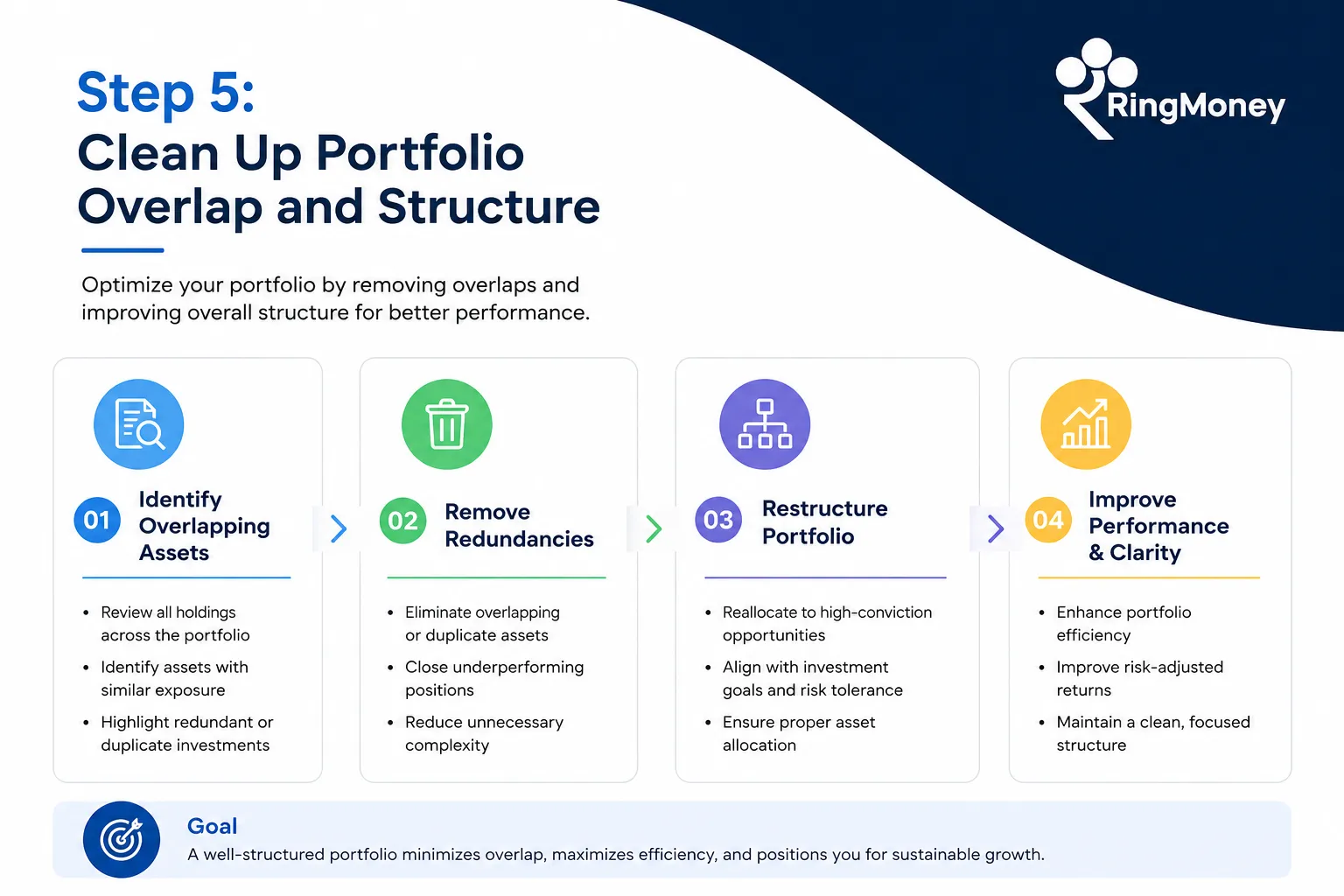

Underperformance is often not just about one fund. It can be a symptom of a poorly structured portfolio.

Many investors unknowingly hold multiple funds that invest in the same underlying stocks. This creates redundancy rather than diversification.

Use this quick structural checklist to scan your portfolio for underlying vulnerabilities:

Checkpoint | What to Look For |

Fund Overlap | More than 50–60% similarity across holdings |

Category Duplication | Multiple funds serving the same role |

Risk Imbalance | Too much exposure to a single market segment |

A focused portfolio of well-chosen funds often performs better than a scattered one with many similar schemes.