Not always. Having too many SIPs isn’t automatically a problem, but if several of them invest in the same companies, they can make your portfolio more complicated without adding much value.

Think about your own journey. You started one SIP when you got your first job. Later, you added another after a salary hike. A friend recommended a fund, your bank suggested one, and an investment app promoted another. Before you knew it, you were managing 10 or 15 SIPs.

It may look like you’re well diversified, but that’s not always true. Many mutual funds invest in the same companies, so you could simply be buying the same stocks multiple times.

The real question isn’t how many SIPs you have. It’s whether each one has a clear purpose. This guide will help you decide if it’s time to consolidate your SIPs and how to do it the right way.

Why So Many Investors End Up With Multiple SIPs

Most people don’t plan to have 10 or 15 SIPs. It usually happens one small decision at a time.

You may have started a new SIP because:

- Your salary increased, and you wanted to invest more.

- A friend or family member recommended a fund.

- Your bank or advisor suggested a new scheme.

- An investment app promoted a top-performing fund.

- The market fell, so you invested in another fund instead of increasing an existing SIP.

There’s nothing wrong with any of these decisions. The problem starts when you keep adding new SIPs without reviewing the ones you already have. Over time, your portfolio becomes crowded, and it gets harder to track what each fund is actually doing.

Is Having Many SIPs Really a Problem?

It depends.

The number of SIPs isn’t the problem. What those funds invest in is what matters.

For example:

- 5 SIPs can be perfectly fine if each fund serves a different purpose.

- 10 SIPs can be a problem if most of them invest in the same companies.

Here’s the key point:

More mutual funds don’t automatically mean more diversification.

You could be buying the same stocks through different fund managers without realising it. Instead of spreading your risk, you’re simply creating duplicate investments.

That’s the mistake many SIP investors unknowingly make.

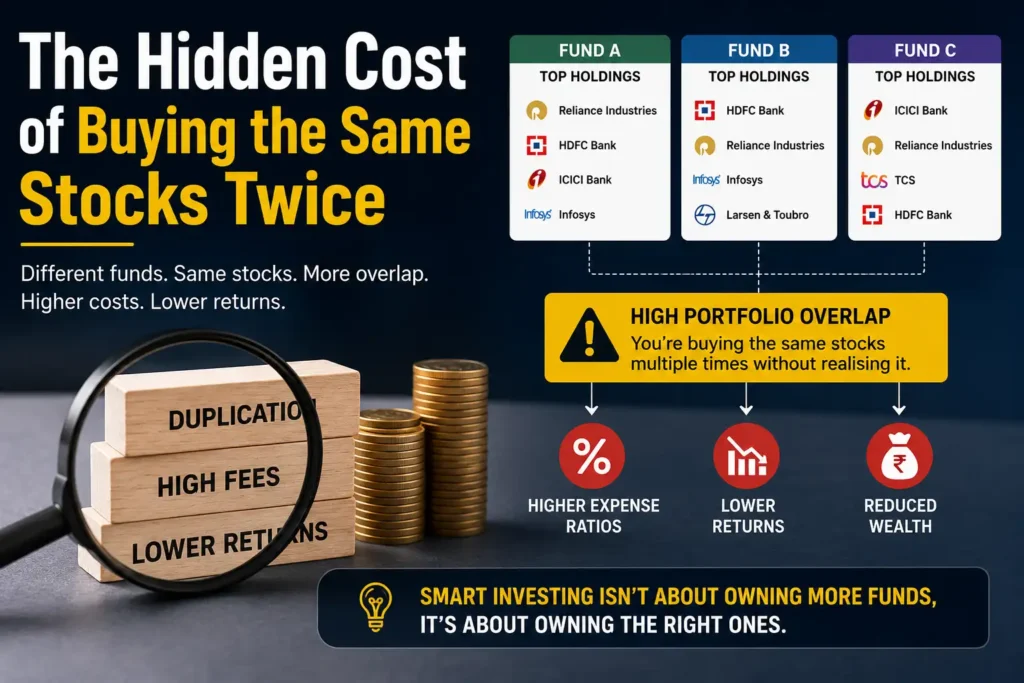

The Hidden Cost of Buying the Same Stocks Twice

One of the biggest myths is that different mutual fund names mean different investments. That’s often not true.

Here’s a simple example:

Fund | Top Holdings |

Fund A | Reliance Industries, HDFC Bank, ICICI Bank, Infosys |

Fund B | HDFC Bank, Reliance Industries, Infosys, Larsen & Toubro |

Fund C | ICICI Bank, Reliance Industries, TCS, HDFC Bank |

Notice the pattern? Reliance Industries, HDFC Bank, and ICICI Bank appear in multiple funds.

That means even though you’re investing through three different SIPs, a large part of your money is still going into the same companies.

This is called portfolio overlap—or simply, buying the same stocks multiple times through different mutual funds.

Some overlap is completely normal, especially in large-cap funds. But when too many funds own the same companies, you’re adding more funds without adding meaningful diversification.

Why More SIPs Don't Always Mean Better Diversification

Many investors believe that more SIPs automatically mean better diversification. In reality, diversification is about owning different types of investments, not simply adding more mutual funds.

Think of it like a buffet. You fill three plates, but each one has the same rice, chicken, and vegetables. Your table looks fuller, but your meal isn’t any more diverse. The same thing can happen with your portfolio.

A portfolio with 4 well-chosen funds can often provide better diversification than 12 similar funds investing in many of the same companies.

Having too many similar funds can also affect your overall returns. Your best-performing funds are often balanced out by average performers, making it harder for your portfolio to stand out. On top of that, you’re paying multiple expense ratios for funds that may look very similar.

In short, more SIPs don’t always mean more diversification—they can simply mean more duplication.

Five Hidden Problems of Having Too Many SIPs

Owning too many SIPs doesn’t always reduce returns immediately. The bigger impact is often operational and behavioural.

1. Tracking performance becomes confusing

When you have a long list of funds, it becomes difficult to know which ones are actually adding value.

Annual reviews become overwhelming because you’re comparing too many schemes instead of focusing on a handful of meaningful investments.

2. You may accidentally pay for duplicate management

Every actively managed mutual fund charges an annual management fee, known as the Expense Ratio. If you pay a 1% or 1.5% expense ratio to three different large-cap funds that hold identical stock portfolios, you are compounding unnecessary fees that directly eat into your long-term wealth.

3. Emotional decisions become more likely

During market corrections, seeing fifteen funds in red can create unnecessary anxiety.

Many investors stop SIPs randomly instead of reviewing whether the underlying investment thesis has actually changed.

4. Financial goals become unclear

After several years, it’s common to forget why certain SIPs were started.

Was this fund for retirement?

For your child’s education?

For buying a house?

Without clear mapping between investments and goals, portfolio management becomes guesswork.

5. Tax reporting and paperwork increase

More funds often mean multiple account statements, several capital gains reports, and additional effort during tax filing.

While technology has simplified much of this process, fewer well-structured investments are generally easier to manage over the long term.

Expert Perspective: Simplicity Often Wins

Many financial planners suggest that around three to five carefully selected mutual funds are sufficient for most long-term investors. The goal isn’t to collect as many funds as possible but to build a portfolio where every investment has a clear role and minimal unnecessary duplication.

This isn’t a rigid rule.

Your ideal number depends on your financial goals, risk tolerance, investment horizon, and asset allocation.

However, beyond a certain point, adding more funds often creates administrative complexity without providing meaningful additional diversification.

How Many SIPs Are Actually Enough?

There is no universal number.

However, many investors can build a well-diversified portfolio using a simple Core and Satellite approach.

Portfolio Role | Typical Category | Purpose |

Core | Index Fund or Flexi Cap Fund | Broad market exposure and long-term stability |

Growth | Mid Cap Fund | Higher growth potential over long investment horizons |

Optional Satellite | Small Cap, Hybrid or Debt Fund | Additional diversification based on goals and risk appetite |

Rather than asking, “How many SIPs should you have?”, ask a better question:

Does each fund have a distinct purpose that another fund isn’t already serving?

If the answer is no, consolidation may deserve consideration.

Before You Stop Anything, Understand This Difference

One of the biggest misconceptions among investors is confusing stopping an SIP with selling investments.

They are completely different actions.

Stopping an SIP | |

Stops future monthly investments | Sells your existing units |

Existing investments remain invested | Money comes back to your bank account |

No capital gains tax simply for stopping the SIP | Selling may trigger capital gains tax |

No exit load just for stopping the SIP | Exit load may apply depending on the holding period |

This distinction matters because many investors panic unnecessarily.

Stopping future investments is often the first step in consolidation. Selling existing investments requires more careful analysis.

Should You Redeem Old Funds?

Not always.

In many situations, stopping unnecessary SIPs and redirecting future investments into your stronger core funds is enough.

Redeeming should only happen after reviewing factors such as:

- Exit load: Some equity funds charge an exit load if units are redeemed within a specified period, commonly one year. Waiting until this window ends could reduce friction costs.

- Capital gains tax: Selling investments can create tax implications depending on how long you’ve held the units and the applicable tax rules.

In many tax jurisdictions, holding equity units for over 12 months qualifies them for Long-Term Capital Gains taxation, which features lower tax rates—and often a tax-free baseline up to a specific limit each financial year—compared to short-term redemptions.

- Fund quality: A good fund shouldn’t be sold simply because you have too many funds.

- Your financial goals: If a fund still supports an important long-term objective, consolidation may not require selling it immediately.

Sometimes the smartest approach is gradual simplification rather than aggressive restructuring.

Quick Checklist: Does Your Portfolio Need Consolidation?

Review the following statements honestly.

- □ You have more than seven active SIPs.

- □ You own multiple funds from the same category.

- □ Several funds invest in similar large companies.

- □ You no longer remember why some SIPs were started.

- □ Reviewing your portfolio feels overwhelming.

- □ You struggle to identify which fund is performing best.

- □ Your investments aren’t linked to specific financial goals.

If three or more statements apply, it may be a good time to conduct a structured portfolio review.

That doesn’t automatically mean reducing funds immediately.

It means understanding whether every SIP still deserves a place in your investment plan.

How to Consolidate Your SIPs Without Hurting Your Portfolio

Portfolio consolidation should be thoughtful rather than emotional. Follow a structured approach.

Step 1: List every mutual fund

Create a complete inventory of your SIPs, categories, investment amounts, and original objectives.

Step 2: Group similar funds together

Identify funds that belong to the same category and appear to follow similar investment strategies.

Step 3: Look for unnecessary duplication

Review the major holdings and determine whether you’re repeatedly investing in the same companies.

Step 4: Identify your core portfolio

Keep funds that align with your long-term goals and offer distinct exposure.

Step 5: Stop unnecessary SIPs first

If duplication exists, pause future investments before considering redemption.

Step 6: Review once a year

Avoid making frequent changes.

An annual review is usually sufficient unless your financial goals or personal circumstances change significantly.

Common Myths About Multiple SIPs

Myth: More SIPs always generate higher returns.

Reality: Returns depend on the quality of your investments, not the number of SIPs.

Myth: Every new mutual fund improves diversification.

Reality: Different funds can still invest in many of the same companies.

Myth: Stopping an SIP means losing your investment.

Reality: Your existing units continue to remain invested unless you redeem them.

Myth: You should immediately sell duplicate funds.

Reality: Selling without considering taxes, exit load, and long-term goals can do more harm than good.

How RingMoney Can Help

Reviewing multiple SIPs on your own can be confusing, especially when you’re unsure which funds to keep and which ones may be overlapping.

With RingMoney, you can get a clearer view of your mutual fund portfolio, understand where unnecessary duplication may exist, and make more informed investment decisions. Instead of adding more funds, you can focus on building a portfolio that’s simple, goal-oriented, and easier to manage over the long term.

The Lesson Most Investors Learn Too Late

The biggest risk in your portfolio may not be a market crash.

It could be owning investments you no longer understand.

Many investors can tell you exactly how many SIPs they have, but not why they started each one. That’s a warning sign. Every fund in your portfolio should have a clear job. If you can’t explain its purpose in a sentence, it may not deserve your next monthly investment.

Before starting another SIP, ask yourself one simple question:

“Am I adding something new to my portfolio, or just adding another fund?”

That one question can save you years of unnecessary complexity, duplicate investments, and avoidable costs. Sometimes, the smartest investment decision isn’t starting a new SIP—it’s knowing when not to.

Frequently Asked Questions

Can you have multiple SIPs in the same mutual fund?

Yes. Many investors start separate SIPs in the same fund for different goals or on different dates. While it’s allowed, combining them can make your investments easier to manage.

Should you consolidate SIPs during a market downturn?

Generally, avoid making consolidation decisions based only on market movements. Review your portfolio when you’re calm, so your decisions are driven by strategy rather than fear.

Does having more SIPs improve your credit score or financial profile?

No. SIPs have no impact on your credit score because they aren’t loans or credit products. They only reflect your investment habits, not your borrowing history.

How often should you review your SIP portfolio?

A detailed review once a year is usually enough. You should also review it after major life events, such as a job change, marriage, or achieving an important financial goal.

Can you transfer an SIP from one mutual fund to another?

Not directly. You can stop an existing SIP and start a new one in another fund. If you also want to move your invested money, you’ll need to redeem the old units and invest again, keeping taxes and exit load in mind.