If you’ve inherited mutual funds from a parent, the first thing you should know is this: India does not have an inheritance tax. Simply receiving mutual fund units from your parent does not create an immediate tax liability.

However, taxes may apply later when you redeem or sell those units. At the same time, you’ll need to complete the transmission process to transfer the investments into your name.

For many families, these become urgent questions during an already difficult time. Understanding the difference between transmission and taxation can help you avoid delays, unnecessary paperwork, and costly mistakes.

In this guide, you’ll learn how the mutual fund transmission process works, how inherited mutual funds are taxed in India, key mistakes to avoid, and how RingMoney can help you track, manage, and grow inherited investments more efficiently.

The Biggest Relief First: India Has No Inheritance Tax

No. Inheriting mutual funds does not create a tax liability because the transfer is treated as a transmission, not a sale.

During transmission, the mutual fund units simply move from the deceased investor’s name to the rightful claimant. Since no units are redeemed and no gains are realized, no tax is triggered at this stage.

Any tax liability arises only when you later sell or redeem the inherited units.

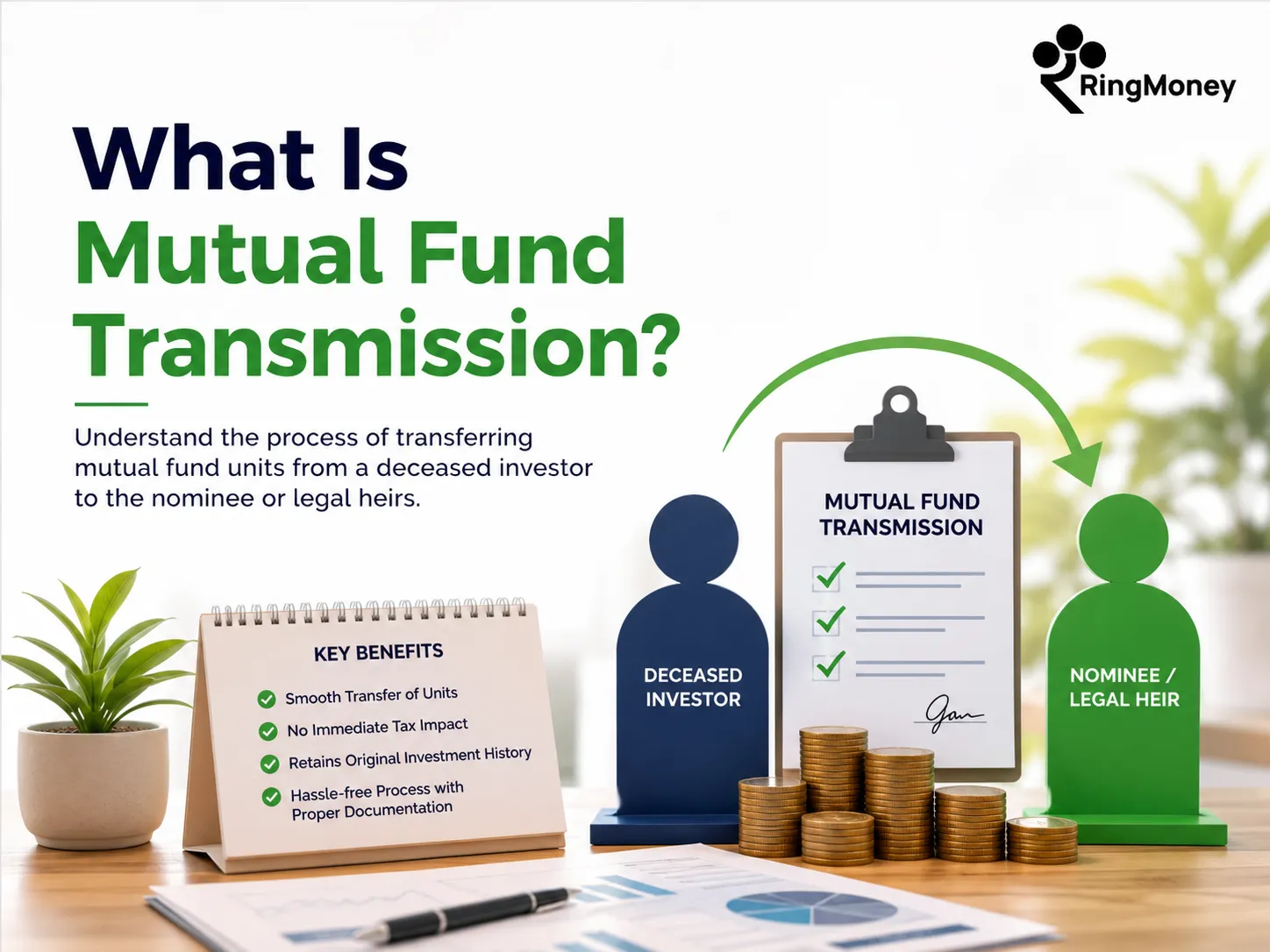

What Is Mutual Fund Transmission?

Transmission is the process of transferring mutual fund units from a deceased investor’s folio to the nominee, surviving joint holder, or legal heir.

Think of it as an ownership update rather than an investment transaction.

The mutual fund units continue to exist exactly as before. Their purchase history, acquisition cost, and holding period remain intact. The only thing that changes is the name of the owner.

The process is generally handled through the fund house’s Registrar and Transfer Agent (RTA), usually CAMS or KFintech, depending on the AMC.

How Do You Transfer Inherited Mutual Funds Into Your Name?

The exact process depends on whether your parent had registered a nominee and the value of the mutual fund holdings.

Path 1: When a Nominee Is Registered

This is the simplest and fastest route.

If your parent had nominated you, you’ll typically need to submit:

- Death certificate of the investor

- Transmission Request Form (Form T3)

- PAN card copy

- KYC documents

- Cancelled cheque of the claimant

- Signature attestation, where applicable

After verification, the units are transferred to your existing folio or a newly created folio in your name.

Most AMCs and RTAs complete transmission within approximately 15 working days when all documents are submitted correctly.

Path 2: No Nominee and Holdings Within Simplified Limits

If your parent did not register a nominee, you may be able to avoid court proceedings altogether if the holdings fall within the prescribed limits: up to ₹5 lakhs per folio for physical/SOA mutual funds or up to ₹15 lakhs for Demat-held mutual funds.

You may need to submit:

- Death certificate of the investor

- Indemnity bond and legal heir affidavits

- No Objection Certificates (NOCs) from other legal heirs

- PAN, KYC, and bank account proof of the claimant

Path 3: No Nominee and Holdings Above Simplified Limits

If the holdings exceed ₹5 lakhs per folio (physical/SOA) or ₹15 lakhs (Demat), the AMC will generally require court-issued documents before processing the transmission.

Depending on the case, you may need:

- Succession Certificate

- Probate of Will

- Letter of Administration or a court order establishing legal heirship

Quick Overview: Documents Required

Situation | Value Threshold | Key Documents Required |

Nominee Registered | Any Amount | Death Certificate, Form T3, PAN, KYC, Bank Cancelled Cheque |

No Nominee Registered | Up to ₹5 Lakhs (SOA) / ₹15 Lakhs (Demat) | Death Certificate, Indemnity Bond, Family NOCs, Legal Heir Affidavits |

No Nominee Registered | Above ₹5 Lakhs (SOA) / ₹15 Lakhs (Demat) | Death Certificate, Succession Certificate, Probated Will, or Letter of Administration |

When Do You Actually Pay Tax?

Here’s the most important rule to remember:

You inherit not only the mutual fund units, but also their financial history.

This means two crucial things transfer from your parents to you:

- Original purchase date

- Original purchase cost

The tax department does not reset the investment history simply because ownership changed through inheritance.

As a result, when you eventually redeem the units, your capital gains are calculated using your parents’ original investment details.

Understanding Tax on Inherited Equity Mutual Funds

Equity mutual funds receive different tax treatment depending on the overall holding period.

The holding period starts from the date your parent originally invested, not from the date you inherited the units.

Equity Fund Scenario | Tax Treatment |

Holding Period Up To 12 Months | Short-Term Capital Gains (STCG) taxed at 20% |

Holding Period Above 12 Months | Long-Term Capital Gains (LTCG) taxed at 12.5% |

LTCG Exemption | First ₹1.25 lakh of annual gains remains exempt |

Example

Suppose your parent invested ₹5 lakh in an equity mutual fund in 2019.

By 2026, the investment grows to ₹12 lakh and is transmitted to you.

If you redeem the units after inheritance:

- Sale Value = ₹12 lakh

- Original Cost = ₹5 lakh

- Capital Gain = ₹7 lakh

Since the holding period began in 2019, the gain qualifies as long-term capital gains.

You can first utilise the annual ₹1.25 lakh LTCG exemption and pay tax only on the remaining eligible gains.

Debt Mutual Funds: The Tax Rule Many Heirs Get Wrong

Debt mutual funds follow a completely different tax framework from equity funds, and the purchase date of the investment is extremely important.

Many heirs assume that all long-term mutual fund investments qualify for the newer 12.5% LTCG tax rate. However, that’s not always true.

Debt Funds Purchased Before April 1, 2023

These investments continue to follow the legacy tax regime.

Holding Period | Tax Treatment |

Up to 36 Months | Short-Term Capital Gains (STCG) are taxed at your income tax slab rate |

More Than 36 Months | Long-Term Capital Gains (LTCG) are taxed at 20% with indexation benefits |

Indexation allows you to adjust the purchase cost for inflation, which can significantly reduce your taxable gains. For long-held debt fund investments inherited from a parent, this benefit can result in substantial tax savings.

Debt Funds Purchased On or After April 1, 2023

The rules changed significantly for debt mutual funds purchased from April 1, 2023, onward.

Regardless of how long the investment was held:

- Gains are added to your taxable income.

- Tax is charged according to your applicable income tax slab.

- No indexation benefit is available.

- No long-term capital gains treatment applies.

This distinction is particularly important when you inherit older debt fund investments from a parent. Before redeeming any inherited debt fund units, verify the original purchase date. A debt fund bought in 2022 may qualify for indexation benefits and 20% LTCG taxation, while an otherwise identical investment purchased in 2024 would be taxed entirely at your slab rate.

Getting this detail wrong can lead to a significant miscalculation of your actual tax liability.

The Nominee Trap Most Families Don't Understand

One of the most misunderstood concepts in financial inheritance is the role of a nominee.

Many people believe that a nominee automatically becomes the owner of the investment.

Legally, that isn’t always true.

A nominee is generally considered a custodian who receives the assets and facilitates their transfer to the rightful legal heirs according to succession laws or a valid Will.

Why does this matter?

Because if the nominee and legal heir are different individuals, complications can arise.

In certain situations, assets may need to be redirected to the rightful heir. Fortunately, under recent SEBI guidelines, RTAs now use a specialised “TLH” (Transmission to Legal Heirs) code to report these inward movements to the tax department, ensuring the process remains completely tax-exempt for the nominee. However, shifting units still creates operational delays

This is why financial experts consistently recommend aligning:

- Your nominee details

- Your Will

- Your intended beneficiaries

When these three elements match, families typically experience a much smoother transmission process.

An Overlooked Tax Benefit: Grandfathering for Older Equity Investments

If your parent invested in equity mutual funds before January 31, 2018, an important grandfathering provision may apply.

Under these rules, capital gains calculations may consider the January 31, 2018, valuation when determining taxable gains.

For long-held family portfolios, this can substantially reduce the eventual tax burden.

Many heirs never realise this benefit exists and end up overestimating their future tax liability.

Before redeeming inherited equity funds purchased before 2018, it’s worth reviewing historical NAV records and consulting a qualified tax professional.

Important: Before redeeming inherited mutual funds, calculate the gains carefully. In many cases, spreading redemptions across multiple financial years allows you to utilise the ₹1.25 lakh annual LTCG exemption repeatedly, potentially reducing your overall tax burden.

Managing Multiple Inherited Investments Can Be Complicated

One challenge many heirs face is simply locating and tracking all inherited investments.

Your parent may have invested through different AMCs over many years. Some folios may sit with CAMS, others with KFintech, and some investments may have been made through different distributors altogether.

As a result, families often spend weeks trying to piece together a complete picture of inherited assets.

This is where modern investment platforms become extremely valuable.

Why RingMoney Is the Best Mutual Fund App for Managing and Growing Your Investments

Once inherited units are successfully transmitted to your name, the next decision is equally important: how will you manage them going forward?

At RingMoney, we believe investing should be simple, transparent, and accessible, especially during moments when financial complexity is the last thing you need.

RingMoney helps you move beyond scattered statements and fragmented portfolios by providing a seamless investment experience in one place.

With RingMoney, you can:

- Track your mutual fund investments through a single intuitive dashboard

- Instantly import your parents’ old Consolidated Account Statement (CAS) to bring scattered, decades-old portfolios into one modern dashboard.

- Track original purchase dates automatically, showing you exactly which inherited units are safely inside the tax-free ₹1.25 Lakh annual profit window.

- Invest across top mutual fund categories with ease

- Stay organised without juggling multiple platforms

- Make smarter long-term wealth-building decisions

Whether you’ve inherited investments or are building wealth for future generations, RingMoney offers a user-friendly experience designed to help you stay in control of your financial journey.

For investors looking for simplicity, convenience, and a modern investing experience, RingMoney stands out as one of the best mutual fund apps available today.

Three Things You Should Do Right Now

If you’ve inherited mutual funds from a parent:

- Identify all mutual fund holdings and gather the relevant folio details.

- Complete the transmission process before making any redemption decisions.

- Understand the tax implications before selling or redeeming units.

If you’re planning your own estate, take a few simple steps today:

- Add nominees to every mutual fund folio.

- Ensure your Will and nominations are aligned.

- Keep an updated record of your investments and folio details.

- Review nominations after major life events such as marriage, divorce, or the birth of a child.

At RingMoney, we believe wealth should be easy to track, manage, and pass on. Whether you’re managing inherited investments or building long-term wealth for your family, RingMoney helps you stay organised and invest with confidence.

Frequently Asked Questions

Can I continue my parents' SIP after inheriting the mutual funds?

No. SIP registrations are linked to the original investor and stop after their death. Once the units are transmitted, you can start a new SIP in your own name if you wish to continue investing.

What happens if my parent had mutual funds across multiple AMCs?

You’ll need to submit separate transmission requests to each AMC or its RTA. Obtaining a Consolidated Account Statement (CAS) can help you identify all holdings in one place before starting the process.

Can I switch inherited mutual fund units to another scheme without redeeming them?

Yes, but a switch is treated as a redemption and fresh purchase for tax purposes. Before making any switches, evaluate the potential capital gains tax impact.

What if I cannot find all of my parent's mutual fund folios?

You can request a Consolidated Account Statement using your parents’ PAN and registered details. This often helps uncover investments spread across multiple fund houses.

Should I redeem inherited mutual funds immediately?

Not necessarily. Before redeeming, review the fund’s performance, asset allocation, and tax implications. In many cases, a planned approach may be more beneficial than an immediate withdrawal.