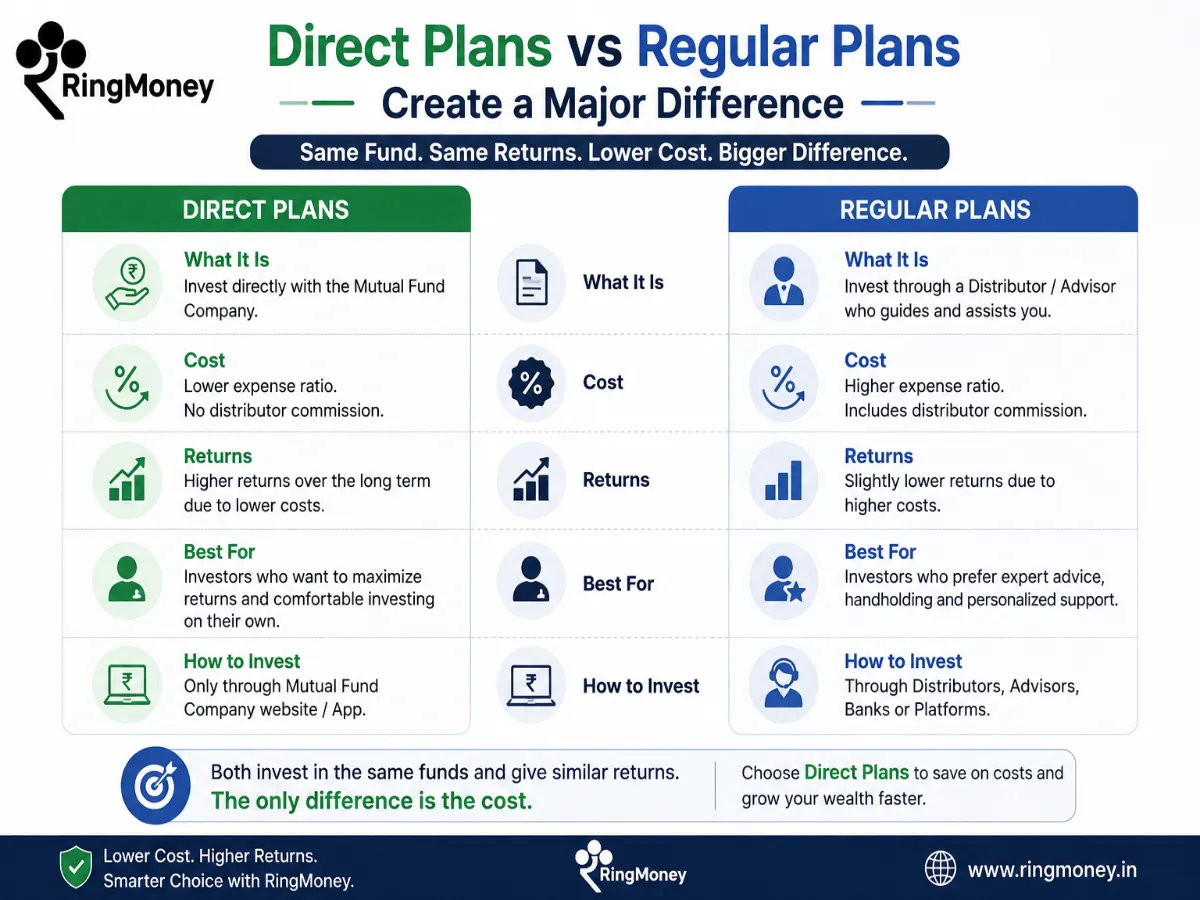

One of the biggest reasons behind unequal returns is the difference between Direct Plans and Regular Plans. Most investors underestimate how much this single factor affects long-term wealth.

Every mutual fund generally offers two versions of the same scheme:

Plan Type | How It Works | Expense Ratio | Long-Term Impact |

Direct Plan | Investment made directly with the AMC | Lower | Higher net returns |

Regular Plan | Investment routed through distributors or agents | Higher | Lower net returns |

The portfolio holdings remain the same in both plans. The fund manager is the same. The strategy is the same. The only major difference is cost.

Regular plans include distributor commissions inside the expense ratio. This commission is deducted silently every year from the investor’s money. Investors usually never notice it because the deduction happens internally before returns are reflected in the NAV.

At first glance, a 1% higher expense ratio may not seem meaningful. But compounding changes everything.

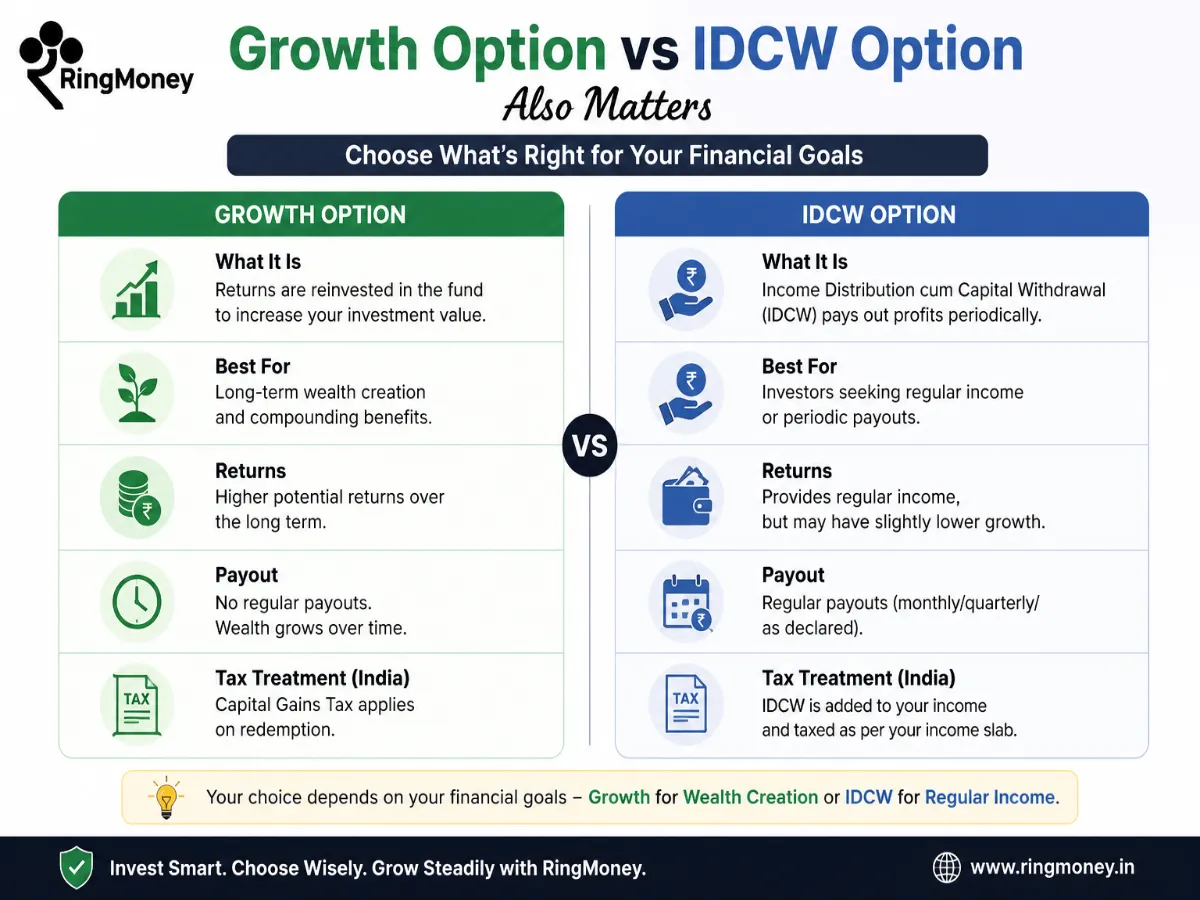

Mutual funds generally offer two payout structures:

Option | What Happens to Profits |

Growth Option | Profits remain invested and compound |

IDCW Option | Profits are periodically distributed |

In the Growth option, earnings automatically stay invested inside the fund. This allows compounding to work continuously over long periods.

In IDCW options, payouts are distributed instead of reinvested. As a result, the invested base grows more slowly.

Two investors may hold the same mutual fund, but if one selected the Growth option and the other chose IDCW, their final portfolio values can differ substantially over time.

For long-term wealth creation, the Growth option generally provides stronger compounding potential.