Picking the right mutual fund option might seem like no big deal, just some paperwork thing. But it actually affects how your money grows over the years. Folks often mess up choosing between Dividend Reinvestment—or IDCW Reinvestment—and the Growth Option.

Both keep your cash in the same fund. Thing is, taxes hit different and that changes your long-term pile-up a lot.

Getting this straight matters if you’re doing SIPs or planning for the long haul.

Why This Choice Matters More Than Most Investors Think

At first glance, Dividend Reinvestment appears similar to the Growth option. The dividend declared by the fund is automatically used to purchase additional units, so the money stays invested.

But the crucial detail many investors overlook is tax timing.

With Dividend Reinvestment, every dividend declaration becomes an immediate taxable event, even if the investor never receives cash. In contrast, the Growth option defers taxation entirely until the investor sells the units.

This difference creates what financial planners often call “tax leakage.”

Understanding the Two Options

Before diving into the tax side of things, it’s worth getting a handle on how these options actually play out.

Dividend Reinvestment (IDCW Reinvestment)

When the fund pays out a dividend:

- They send the amount your way.

- But instead of cash hitting your account, it goes right back into buying more units of that fund.

Thing is, you still get taxed on it at whatever your income slab is—even if the money never leaves the investment.

Growth Option

In the Growth option:

- No dividends are declared.

- All profits remain within the fund and are reflected in the rising Net Asset Value (NAV).

- Taxes are paid only when units are redeemed.

This structure allows the entire investment to continue compounding without interruption.

Key Tax Differences at a Glance

Feature | Dividend Reinvestment (IDCW Reinvestment) | Growth Option |

Tax Trigger | Every time a dividend is declared | Only when units are redeemed |

Tax Rate | Investor’s income tax slab | Capital gains tax |

TDS Applicability | 10% TDS if dividends exceed ₹5,000 | No TDS during the investment period |

Compounding Efficiency | Reduced due to tax deductions | Fully uninterrupted compounding |

Investor Control Over Tax Timing | Low (AMC decides dividend timing) | High (investor decides redemption timing) |

This difference in tax structure directly affects how much money remains invested over time.

The FIFO Complexity Investors Often Miss

Dividend reinvestment creates multiple tiny purchase transactions each time a dividend is declared and reinvested. When you eventually sell units, tax calculations follow the First-In-First-Out (FIFO) rule, which means every reinvested dividend has a different purchase date and cost. This can make capital gains calculations and tax reporting significantly more complicated compared to the cleaner purchase timeline of a Growth-option SIP.

The Hidden Cost: Tax Leakage in Dividend Reinvestment

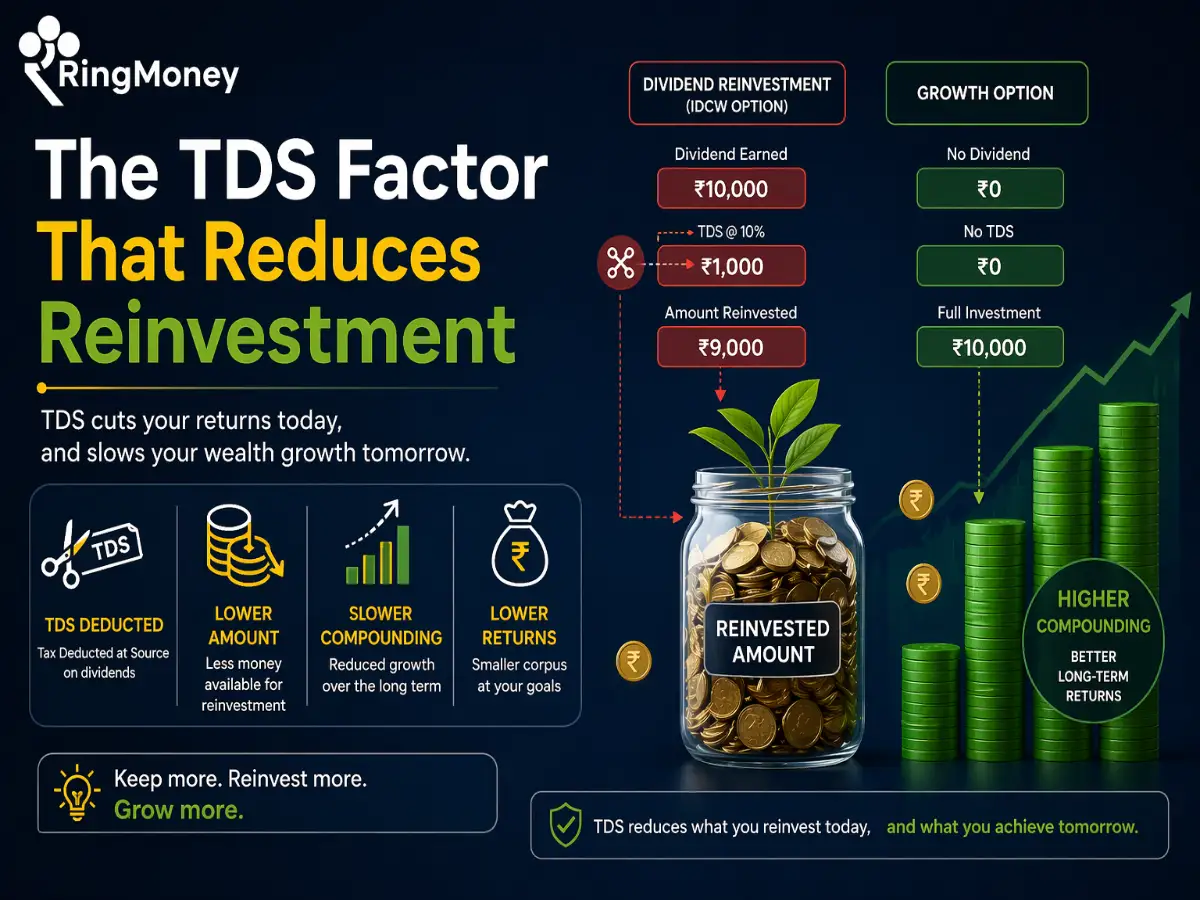

Dividends from mutual funds get taxed right away, based on whatever slab your income falls into—could hit 30% if you’re in a higher one.

That bites because part of that dividend just doesn’t come back into your pocket or the investment.

Say you get a ₹10,000 dividend, and you’re at 30% tax. Bam, ₹3,000 goes to tax. You’re left putting just ₹7,000 back, even though the fund spat out ₹10,000 worth of gains from your money.

Do that over the years, and all those nibbles keep shrinking what you’ve got working for you through compounding.

The Compounding Advantage of the Growth Option

The Growth option avoids this recurring tax event.

Instead of distributing profits, the fund retains them, allowing the full amount to continue generating returns. Taxes are paid only when the investor chooses to redeem units.

This structure creates tax-deferred compounding, which is a powerful long-term advantage.

For equity mutual funds in India:

- Short-term capital gains? That’s 15% if you sell within a year.

- Long-term ones hit 10% on anything over ₹1.25 lakh yearly, after holding a year.

Way better than the 30% that could slap dividends.

Plus, you pay later – let your money grow full steam for years first.

Latest tax setup

Now it’s 20% on short-term gains for these funds, 12.5% on long-term over that ₹1.25 lakh bit. Still, capital gains tax beats out dividend hits at your slab rate most times, even tweaked like this.

The NAV Adjustment: Many Investors Misinterpret

Another commonly misunderstood aspect involves the Net Asset Value (NAV).

When a mutual fund declares a dividend, the NAV of the scheme falls by the exact dividend amount.

This means the dividend is not additional profit. Instead, it is essentially capital being distributed from the fund’s value.

In the Dividend Reinvestment option, investors are not just paying tax on their own money; they are also losing the future compounding power of that tax amount permanently, which quietly reduces long-term portfolio growth.

In simple terms:

- The fund’s NAV decreases.

- The dividend amount is paid or reinvested.

- A tax event is triggered.

The investor ends up paying tax merely to shift money from the fund’s NAV back into units.

The TDS Factor That Reduces Reinvestment

There is another layer that many investors miss.

If dividend income from a mutual fund exceeds ₹10,000 in a financial year, per AMC, the fund house deducts 10% TDS (Tax Deducted at Source) before distributing the dividend. In a reinvestment plan, this means the entire dividend amount is not reinvested because a portion is deducted as tax first.

This further reduces the number of units purchased compared to what investors may expect.

When Dividend Reinvestment Might Make Sense

Although the Growth option is generally more tax efficient, Dividend Reinvestment may still suit certain investors.

Examples include:

- Investors in very low tax brackets

- Individuals relying on regular income from investments

- Situations where locking in gains at current tax rates may be beneficial

However, for most long-term investors focused on wealth accumulation, the Growth option usually delivers better results.

Why Long-Term Investors Often Prefer the Growth Option

From a purely financial perspective, the Growth option offers several advantages:

- No annual tax interruptions

- Higher capital available for compounding

- Control over when tax is paid

- Lower tax rates compared to slab-based dividend taxation

Over a 10–20 year investment horizon, these factors can translate into a substantial difference in final portfolio value.

Managing Tax-Efficient SIP Investments

Understanding these nuances is only part of the process. Investors also need a platform that makes long-term investing simple, transparent, and efficient.

That is where we focus heavily on simplifying the experience through RingMoney.

With RingMoney, investors can:

- Start and manage SIPs seamlessly

- Track mutual fund portfolios in one place

- Focus on long-term growth-oriented investing strategies

- Invest with clarity rather than confusion

Our goal is to ensure that investors do not lose wealth due to hidden tax inefficiencies or complicated investment interfaces.

The Strategic Takeaway

Dividend Reinvestment and the Growth option may appear similar on the surface, but the tax treatment creates a meaningful difference.

Dividend Reinvestment hits you with taxes right away at your slab rate, so less cash ends up getting put back in. Growth option lets those profits just keep compounding without the tax bite until you cash out.

For folks aiming to pile up wealth over time with mutual funds or SIPs, going Growth for that tax-deferred growth usually works better.

Pair it with something straightforward like RingMoney, and managing the whole thing gets way easier—you can just focus on sticking to long-term gains.

Read More:

Frequently Asked Questions

Is Dividend Reinvestment the same as the Growth option?

No. While both options keep money invested in the fund, they differ in how taxes are applied. Dividend Reinvestment creates a taxable event every time a dividend is declared, whereas the Growth option allows profits to remain invested without taxation until redemption.

Why do some investors still choose the dividend option?

Some investors prefer dividend options when they want periodic income from their investments. It may also appeal to those who like seeing payouts, even if they are reinvested. However, this preference often comes with higher tax implications.

Does the NAV change when a dividend is declared?

Yes. When a mutual fund declares a dividend, the NAV of the scheme falls by the same amount as the dividend distributed. This means the dividend is not additional profit but rather a portion of the fund’s value being paid out.

Can the Growth option help simplify tax planning?Can the Growth option help simplify tax planning?

Yes. Since taxes are triggered only when units are sold, the Growth option gives investors greater control over when they realise gains. This flexibility can make tax planning easier compared to dealing with multiple dividend-related tax entries.

How can investors track and manage the right mutual fund option easily?

Using a dedicated investment platform helps simplify decision-making and portfolio tracking. Platforms like RingMoney allow investors to manage SIPs, monitor mutual fund performance, and stay focused on long-term investment strategies without unnecessary complexity.